S+P futures: biggest weekly rally since April 2020, after falling for seven consecutive weeks

S+P futures rallied 10% from last Friday’s lows to this Friday’s close, DJIA futures were up 8% (2,650 points), NAZ 100 futures rallied 11%, and Russell small-cap futures rose 10%. TSE futures were up 4%.

At last Friday’s lows, S+P futures were down ~21% from their January 4th All-Time Highs, while investor sentiment was the most negative since the Covid Panic lows.

As I noted last week, the S+P doubled from the 2020 lows and is up ~7X from the 2008 lows. Perhaps a correction was due after such spectacular gains.

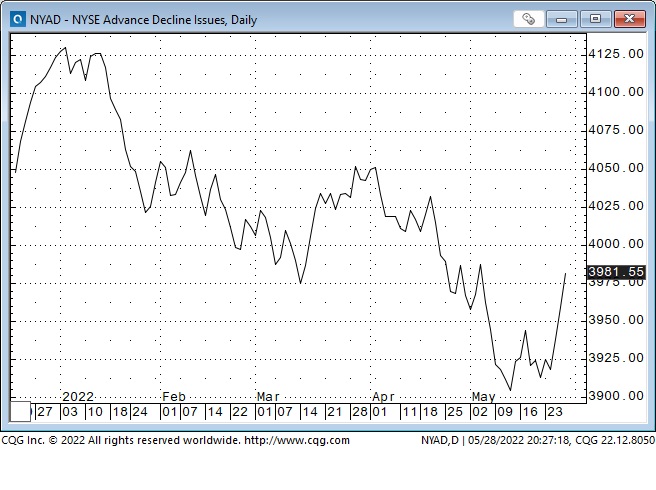

Market breadth was very strong this week, with many more advancing issues than declining issues. The New York Advance-Decline line rose sharply – just like it did during the bear market rally in the 2nd half of March.

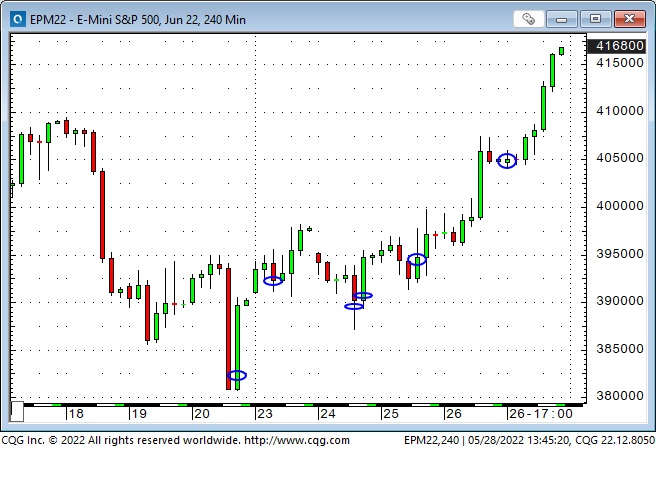

For the past two weeks, I’ve been “bottom-picking” stock index futures. I thought that extreme bearish sentiment plus the “idea” that “peak inflation and peak Fed tightening” may have been “over-priced” set up the possibility of a bear market rally.

Was peak inflation and peak Fed tightening over-priced?

Last fall, when the Fed was still talking “transitory,” the forward markets began to price in Fed tightening in 2022 and 2023. The delta (the rate of change) of that market move accelerated following a brief “Ukraine invasion” hiatus around the end of February, and then the market reversed on May 4.

The June 2023 Eurodollar futures contract priced in a full 300bps of tightening between October 2021 and May 4, 2022 – but has subsequently “taken back” about 55bps. The Eurodollar bounce may be related to the idea that the Fed will be slow to realize the economy is slowing, just as they were slow to realize that inflation was accelerating.

The US Dollar Index has fallen from 20-year highs

I’ve frequently noted that capital flows to the USA for safety and opportunity. The recent risk-off environment that saw stock indices tumble also saw the US Dollar rally as capital sought safety (the USDX rallied ~9% from before the Ukraine invasion to its May 13 highs.) The “opportunity” was the market’s expectation that the Fed would be (much) more aggressive than other Central Banks. (Another important factor is that trends in the FX markets are “self-sustaining” and often run farther than seems to make any sense before turning on a dime.)

However, as the forward market pricing of Fed tightening backed off, the USDX weakened from its May 13 highs.

The inter-market connection

The forward Eurodollar market bottomed on May 4, the 10-year note bottomed three trading days later on May 9, and the US Dollar Index topped out on May 13. These reversals were inspired by the idea that Fed tightening had been over-priced. S+P futures made a 14-month low on May 12, with volatility at a 19-month high. (That was peak vol during the recent 7-week decline. It has trended lower since then, despite the stock indices making a brief lower-low last Friday.)

Energy

The July WTI futures contract closed this week at an All-Time High of $115. (Nearby WTI futures briefly traded above $130 following the Ukraine invasion and Russian sanctions.)

Gasoline futures traded this week at an ATH above $4 (the high in 2008 was ~$3.60 when WTI was $147.)

NYMEX Natgas futures traded above $9 this week for the first time since 2008 – that’s a double from where it was trading in March.

I believe that high energy prices = higher inflation given the “pass-through” effects of high energy prices. I also think that we may have lived through a period from 2015 to 2021 when fossil fuel energy prices were “low” due to greater supply than demand (shale, covid), and now we are in an era when energy prices will be “higher” (increased global demand, low Capex, restrictive ESG inspired government policies.)

But – I know nothing about the energy markets compared to the top people who work in the energy business. This chart is worth a second look.

My short-term trading

I started this week with a long S+P position I bought near last Friday’s lows. (My P+L was down ~0.50% last week as I was “early” trying to “bottom-pick” the stock indices.)

This week I traded the S+P, the Russell and the CAD from the long side. I was stopped for small losses a couple of times but managed to essentially stay long S+P positions into Thursday’s close. I was flat going into the long weekend. My P+L was up ~1.2% on the week.

I covered my long S+P position during the Thursday evening session. It looked like the rally had “run out of gas” mid-way through the Thursday day session.

Thursday trading volumes on all stock index futures were the lowest of the week, (and were dramatically lower than late last week when markets were making new multi-month lows) – DESPITE the HUGE rally. That seemed odd to me.

I covered my long S+P positions because I believed the rally was a bear market counter-trend rally. I recently changed my trading style to “take profits” on counter-trend moves while trying to “stay with” trending moves using trailing stops.

In hindsight, of course, I would have benefited from “staying with” my S+P positions!

I bought the CAD at 7808 early Wednesday, thinking that it would “catch a bid” from the emerging risk-on sentiment in the equity markets, and if it could rally above the recent resistance around 7825-30, it could jump. I was stopped out in the overnight session, but I re-bought it. I covered that position for a small profit early Friday when 7830 seemed to be strong resistance. Shortly after that, CAD caught a bid from equities and energy markets and soared. Trading is not a game of perfect!

On my radar

I think stock indices are having a bear-market rally – a “relief rally” after seven consecutive weeks down. I’m willing to be wrong about that, and I don’t know how far the rally will run, but I think making a new ATH anytime soon is out of the question. (There was WAY too much froth in the market in 2020 – 2021, and people learned about that the hard way. They will now be less inclined to believe “it’s going to the moon.”)

Risk Management

Two weeks ago, a reader in Poland (thank you, Tomasz!) gave me the idea to create a risk management section in my weekly blog. So, each week I will comment on some aspects of what I do and why I do it. I want to emphasize that I make money from trading not because I have a great crystal ball but because I manage risks.

I’m not preaching here, but maybe some readers will get an idea that will benefit their trading.

I have online futures trading accounts with RJOBrien (Canada) funded with less than 5% of my net worth. If RJO suddenly goes out of business, my accounts are covered by CIPF – The Canadian Investor Protection Fund – for up $1 million. (Various American commodity brokerage firms have gone bust in the past 20 years, and clients have lost money.)

I have used CQG software for 25 years, it is regularly updated, and the client service is fantastic. If I have orders placed with RJO via CQG and my computers go down (a power failure, for instance), those orders are “at the exchange” and will remain open. I also have CQG on my cell to see markets and enter orders if my desktop computers and laptop don’t work – or if I’m away from my home office.

I also have access to my RJO accounts by telephone to trading desks in Canada and the USA if my computers and cell are down. Backup to the backup.

I regularly check my CQG Orders and Positions report to confirm my account status and working orders. (It is tough enough to make money trading – losing money because I forgot to enter or cancel an order is a painful mistake!)

If I’ve made a trading mistake, I correct it immediately. Hanging onto an error trade that has (invariably) gone against me, hoping that I can trade out of it at breakeven or better, is DUMB.

I rarely use more than 20% of the capital in my trading account to meet margin requirements.

A high conviction trade is a marketing idea, not a trading plan. I have essentially the same low conviction level on every trade I make. My experience is that more of my trades turn out to be losers than winners, although the losers are usually smaller than the winners. To me, a trade is just a trade.

I pay a lot of attention to intra and inter-market relationships (the correlations between markets) to find trading ideas ( if X and Y are both up what is Z doing?) as well as to be aware of concentration risk ( if I own X and Y and I’m thinking of buying Z will that be more of the same trade?)

Correlations between markets can be strong for a period of time, and then stop working. I will look at correlations for trading ideas and concentration concerns, but I won’t buy X just because Y is going up – the trade has to stand on its own merits.

I don’t want to risk more than 1% of my account capital on a trade. If I’m thinking about making a trade, I need to size it so that if it goes against me, my loss will be less than 1%. If the “proper” stop level is more than 1% away, I won’t make the trade. (The market will be open again tomorrow, and there will be other opportunities.)

When I put on a trade, I usually don’t know where I will take profits, but I do know where I will limit my losses. If I’m buying a market, I will have a “reason” I think it will go up, and that reason will incorporate an amount of potential gain that is worth pursuing, but if the market starts to run, I want to try to say with it.

I almost always enter GTC stop orders immediately after I establish a position. I think of these stops as “worst case” orders, as in, if the market immediately goes hard against me, I will be out at that stop level. Sometimes I will decide that a trade is not working, and I will exit the trade at the market and CXL the stop. I will RARELY ever move a stop to give the market more “room” to go against me. (I will not hang onto a trade because I KNOW I’m right and the trade just needs a little more time before it starts working!)

If I’m long a market and it is trending higher, I will try to find a new stop level to lock in some profits. For example, with the market at its current price, if I bought the market now, where would I put my stop?

I try to keep the time horizon of my trading in sync with the time horizon of my analysis. For instance, if I think crude oil prices will be much higher a year from now, that doesn’t mean that “right now” is a good time to buy crude.

There will be no Trading Desk Notes next week – I will be travelling

The Barney report

People talk about training dogs, but dogs talk about training people. For instance, I’m working at my desk, and I hear a little whimper. I know it’s Barney, so I ignore him, but he whimpers again and will keep it up until I look at him. I know it means he wants attention; maybe rub his tummy, throw one of his toys, or go for a walk – but how can I say no when he looks at me like this?

A request

If you like reading the Trading Desk Notes, please forward a copy or a link to a friend. Also, I genuinely welcome your comments, and please let me know if you would like to see something new in the TD Notes.

Listen to Victor talk about markets

I’ve had a regular weekly spot on Mike Campbell’s extremely popular Moneytalks show for 20 years. The May 28 podcast is available at: https://mikesmoneytalks.ca.

You can listen to my May 14 Howe Street Radio 37-minute interview here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.