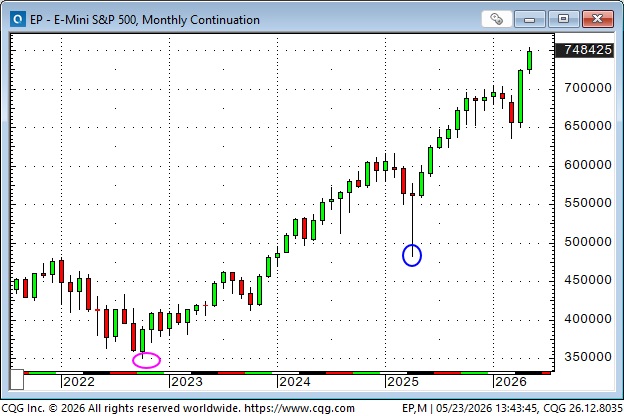

Another all-time high for the S&P, up ~18% from the March lows

The S&P has closed higher for 8 consecutive weeks, something that has happened only 6 times since 1998.

The S&P is up ~56% from the April 2025 “Liberation Day” lows (blue ellipse), and ~115% from the 2022 lows (pink ellipse) when the market began to recover after a series of Fed interest rate hikes.

AAPL is up ~27% from the March lows at new record highs, with a market cap of ~$4.55 trillion. NVDA reported on Wednesday with strong earnings and forecasts, but the share price has fallen slightly. NVDA’s market cap at last week’s highs was nearly $6 trillion.

The SOXX, the semiconductor ETF, reached new record highs this week, even with NVDA selling off.

The S&P market cap is ~$67 trillion. GOOG, AAPL and NVDA = ~$15 trillion market cap, or ~22% of the S&P.

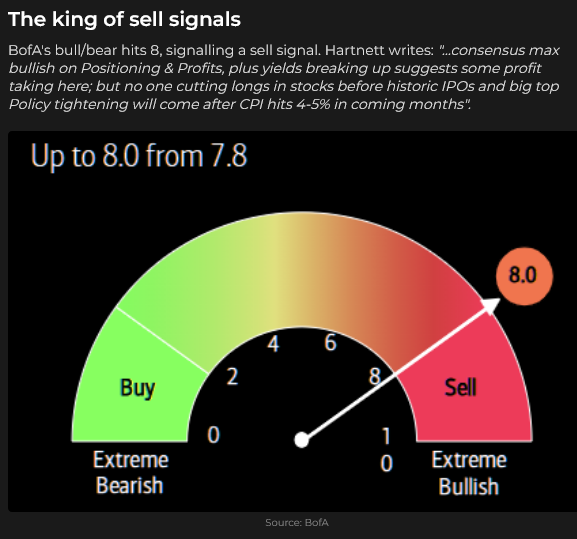

The slow-moving Bank of America Bull/Bear indicator is now signalling a “sell”, but with caveats. Stock market bulls may view a “lack of escalation” in the war with Iran as good news.

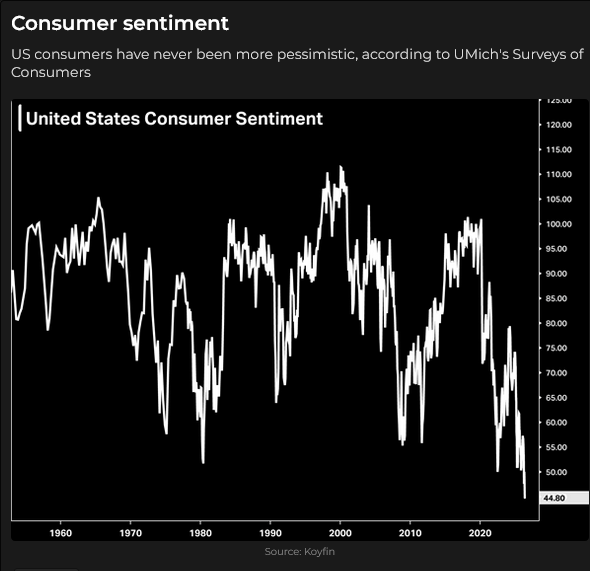

With the stock market at record highs, the University of Michigan’s Consumer Sentiment Survey shows that US consumers have never been more pessimistic. The most common complaint from the people surveyed was the rising cost of living.

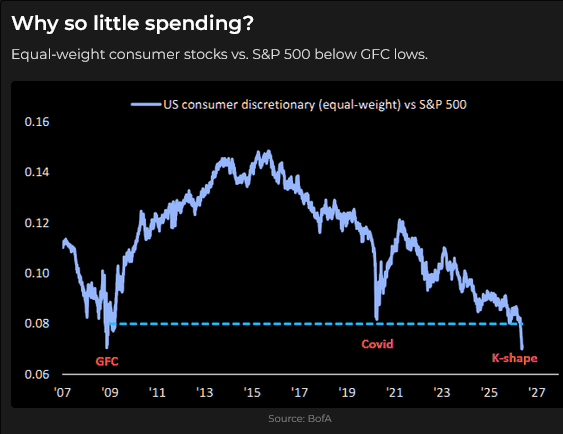

Walmart’s May 21, 2026, Q1 report noted that lower-income consumers were spending less. WMT shares fell on the report.

The “spread” between lower- and higher-income consumers continues to widen and may be a significant factor in the mid-term elections, which are just over 5 months away.

The TSE composite had a record-high weekly close on Friday, up ~11% from the March lows and ~55% from the “Liberation Day” lows in April 2025.

The S&P had its highest daily close last Thursday, May 15, and dropped ~190 points to Tuesday’s lows, as global bond yields surged higher. The market rallied from Wednesday to Friday (blue ellipse) as bond yields declined, but backed off from Friday’s highs ahead of the long Memorial Day weekend and the uncertainty surrounding the war in Iran.

Stock market VOL, as measured by the VIX, nearly doubled from the start of the war to the end of March, then fell sharply in early April as the stock market rallied. VOL has drifted sideways to lower since the 2nd week of April.

Interest rates

The US 30-year Treasury bond futures traded at an 11-month high on March 2, 2026 (blue ellipse) as the war in Iran started (the yield on the 30-year in the cash market was ~4.65%). Global bond prices tumbled as the war continued, with the cash market yield on the US 30-year rising to a 19-year high of ~5.18% at this week’s lows (pink ellipse). The recent sharp rise in bond yields (and bond VOL) may have contributed to the weakness in the S&P from last week’s highs to this week’s lows.

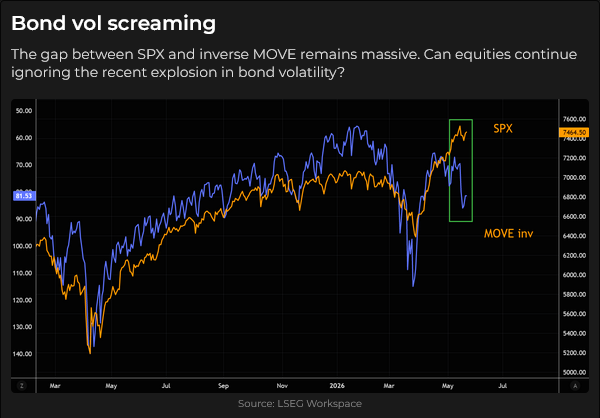

Bond market VOL, as measured by the MOVE index, surged higher throughout March, but then pivoted sharply lower at the end of March as the S&P rallied on expectations of a ceasefire. Recently, bond VOL has turned higher, even as the S&P rallied to new highs. Higher bond VOL and higher bond yields would probably cause stocks to fall. (In this chart, the MOVE index is the blue line with an inverted left-side scale.)

Short-term interest rates also turned higher as the Iran war started (blue ellipse), and have continued to rise, with the December 2026 3-month SOFR futures contract falling nearly 100 bps since then.

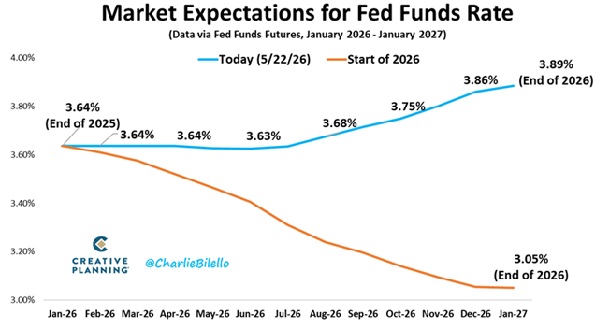

This chart, from Charlie Bilello, shows that before the war started (gold line), the forward market for Fed Funds was pricing ~60 bps of cuts by the end of 2026. Now (blue line), the market is pricing FF ~25 bps higher by the end of 2026.

Kevin Warsh was officially sworn in as Chairman of the Federal Reserve on Friday. Historically, markets “test” a new Fed Chairman early in his first term. Here’s a link to an excellent Substack article about Kevin Warsh, written by my friend (and veteran market analyst and trader) Stephen Innes.

Massive tech IPOs are coming

With global stock markets at or near all-time highs, Wall Street is gearing up for massive IPOs from SpaceX, OpenAI and Anthropic that are expected to “value” the three companies at around $3.5 to $4 trillion. Nasdaq will “fast-track” the companies for inclusion in the Nasdaq-100 Index. Some analysts expect these companies to be “valued” at extraordinary levels on conventional valuation metrics. (Da!)

Crude oil

July Brent futures closed the week at ~$104, down ~$6 from last week’s close. Over the past 4 weeks, July Brent has mostly traded between $100 and $110; in other words, it remains near recent highs, as the crude oil market recognizes that “peace negotiations” do NOT equal a free flow of traffic through the Strait of Hormuz.

Currencies

The DXY US Dollar Index has rallied over the past 2 weeks as US Dollar bulls (like Mark Farrington on Substack) see strong economic growth, strong corporate earnings, rising real rates, and the US dollar’s reserve-currency status contributing to US exceptionalism in the FX market.

The CAD has closed lower for 13 of the last 16 trading days, falling about 1.5 cents as the USD rises against virtually all currencies (because US interest rates are rising faster than those in other countries).

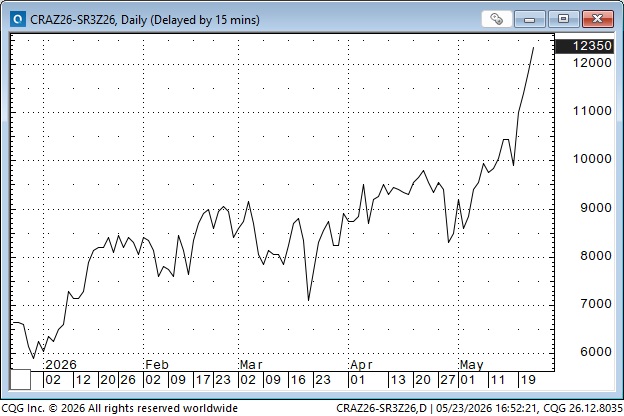

This chart shows the spread between Canadian short-rate futures (CORRA) and US SOFR futures for December 2026. Since late April, the spread delta has widened dramatically as US short rates have risen faster than Canadian short rates. At Friday’s close, US 2-year Treasuries were ~120 bps premium to Canada, and the US 3-month rate was ~138 bps premium to Canada.

Over the last 6 months, the CADUSD rate has traded almost entirely in a 2-cent range between 72 and 74 cents. Over the last 12 months, the CAD has traded between 72 and 74 cents ~80% of the time.

Cuba

The US has charged 94-year-old Raúl Castro with murder, and the world has learned a lot more about GAESA, a paramilitary organization that effectively “runs” Cuba (similar to how the IRGC “runs” Iran). The Donroe Doctrine continues to play out. Link to learn more about GAESA.

My short-term trading

I started this week short the S&P, a position I established Thursday evening last week. I covered the trade for a gain of ~120 points on Tuesday when the bonds and the S&P made new lows and then started to rally.

I kept my long OTM Yen call on the “off-chance” that the Japanese authorities may intervene again to boost the Yen. I entered a GTC sell order above my entry price to take a profit, because if they do “come in,” it will probably trigger a sharp rally while I’m asleep. I don’t want to miss a sharp rally!

I didn’t do much else this week, given the “relentless flow of misinformation” around Iran/USA. Here’s a note I shared with one of my Substack friends:

“I didn’t trade on Friday. I didn’t see anything I wanted to hold into the weekend. I’m trying to make money by managing risk, not by betting that I have a great crystal ball. For entertainment value, not investment advice, my guess on pricing: equity markets probably 80/20 that fighting is over (and even if fighting resumes, equities think it’s “not a big deal.” Bonds are probably 50/50 because the inflation risk from more fighting is a big deal. Crude at $100+ is a great price if the fighting is over, but a ceasefire doesn’t reopen the Hormuz, so there’s a price floor not too far below $100.”

Essentially, I think the markets, especially equity markets, are under-pricing the risk of renewed fighting between the US and Iran. Netanyahu wants to keep fighting. The IRGC doesn’t want to give up the enriched uranium or the nuclear sites, and they want to toll the SOH. That’s a “deal-breaker” for Trump. But what do I know?

On my radar

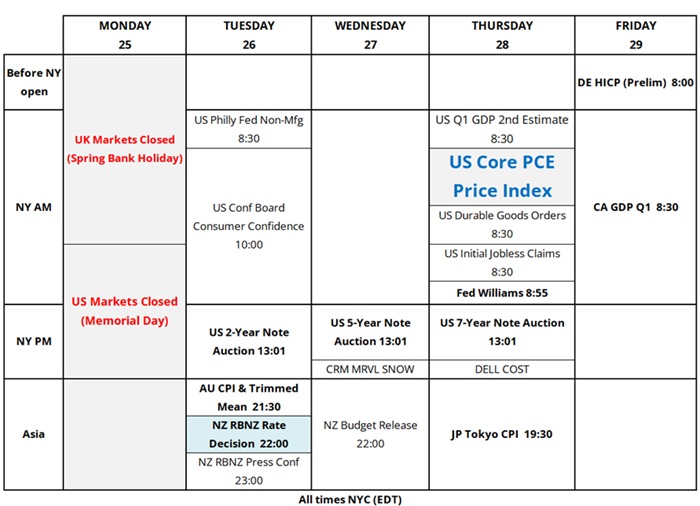

US and UK markets are closed Monday.

The USMCA agreement is up for review starting in July.

Here’s a calendar from Brent Donnelly for next week:

The Barney report

Here’s Barney running towards me at full gallop through 18-inch rough on the golf course outside our house. We’ve been looking for golf balls, and he loves doing that because he gets a treat if he finds one and gives it to me. He’s working for food, and loving it!

Listen to Mike Campbell and me discuss markets

On today’s Moneytalks podcast, Mike and I discussed the high-flying stock market, the surge in bond yields, the new Fed Chair, and the implications of consumer sentiment at multi-decade lows while the stock market makes new highs. You can listen to the entire show here. My spot with Mike starts around the 48-minute mark. Don’t miss my friend Tony Greer and Mike starting at the 5-minute mark.

Listen to Jim Goddard and me discuss markets

I did my monthly 30-minute interview with Jim Goddard on the This Week In Money podcast this morning. We discussed my macro market views and drilled down into what matters for the stock market, rising bond yields, crude oil remaining above $100, the rising US Dollar, metals, the growing “divide” between the rich and the poor, and how my trading has changed during the Iran war. You can listen here. My spot with Jim starts at the 11-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.