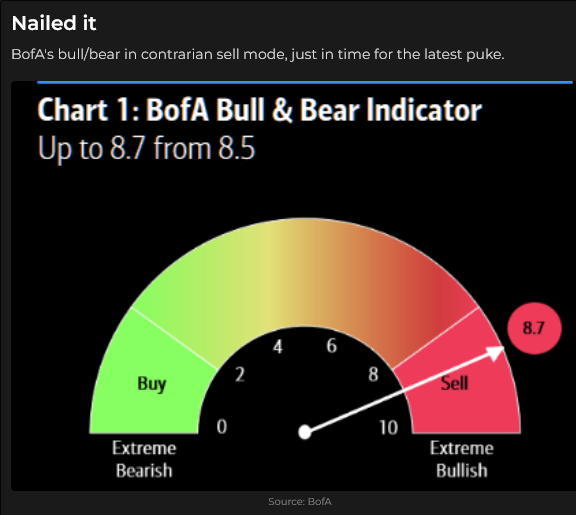

Sooner or later, it was gonna happen

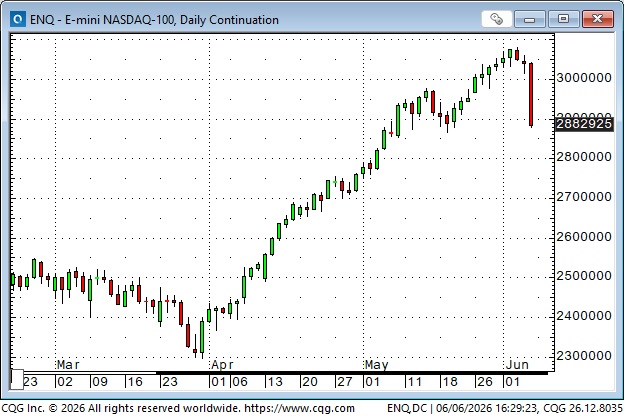

After rallying for 9 consecutive weeks, the leading US stock indices tumbled on Friday.

The weekly S&P chart shows an “outside reversal down” (blue ellipse), which often signals more downside to come (but not necessarily, see the pink ellipse). If the S&P had closed higher this week, that would have been 10 consecutive weeks higher, which hasn’t happened since 1985.

The S&P and many other global indices (and especially several tech stocks) had run “too far, too fast” and were “overdue” for a correction. Various commentators have offered “reasons” for why the correction happened, but from my perspective, it could have been triggered by any number of factors; the “precondition” of being egregiously overbought set the stage for “anything” to trigger a correction.

Dancing near the exit

Citygroup CEO Chuck Prince will forever be remembered for saying, “But as long as the music is playing, you’ve got to get up and dance,” in July of 2007, and that “rule” still applies, but I think a lot of veteran traders have been dancing near the exit, and for good reason.

Global equity markets have had a great run, whether you’re looking at the past 10 weeks or the past 10 years. US household equity wealth has increased by ~$6 trillion YTD (to ~$66 trillion) and is up ~$25 trillion in the last 30 months (since the beginning of 2024).

Investors have learned that dips are great buying opportunities, and since “stocks always go up” (see the passive investors guidebook), then using a little leverage (or a lot) means making more money faster. Buy The DIP (BTD) is more than a mantra, it has become a powerful belief, a self-fulfilling “truth.” (sarcasm alert).

Momentum is king

The trend is your friend, so investors keep paying higher and higher prices, and it has worked like a charm.

Everybody knows (Sincerely, L. Cohen)

That breadth is narrow, that everybody is all-in, that traditional valuation metrics are “stretched,” that a tidal wave of new issues (Tech IPOs) and secondary offerings (GOOG, META and others) are coming, that margin debt is off the charts, that complacency is elevated, that “downside protection” is an “unnecessary” cost, but everybody knows you gotta keep dancing, because you will “miss out” if you don’t.

Bob Farrell

As Bob Farrell told us years ago, rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways.

The looming Tech IPOs – tell me if this sounds familiar

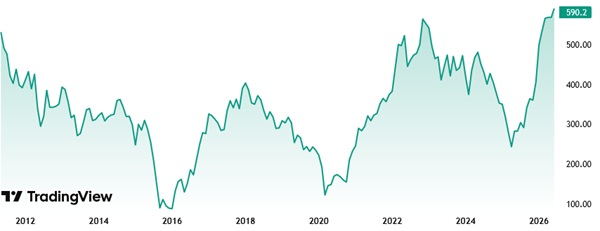

In May 2011, Glencore, the biggest, smartest commodity trading company in the world, went public with a $10 billion IPO (valuing the company at ~$60B). It was universally considered a massive, blockbuster deal at the time, and was over-subscribed. Glencore bypassed standard waiting periods to join the prestigious FTSE 100 Index on its very first day of trading—a rare fast-track move. It was perfect timing for Glencore, right at the top of the 2009 to 2011 commodity bull market, when the Goldman Sachs Commodity Index had more than doubled in two years.

The IPO was done in London at an issue price of 530 pence (GBP). The share price fell dramatically over the next four years, dropping below 100P in the 2015 commodity bear market. It briefly recovered to above the issue price in 2022, then fell back underwater until 2026, and is now (15 years later) at a record high of nearly 600P. However, for a US investor, converting USD to buy GLEN in GBP in 2011, it has never recovered it’s issue price in USD terms because of the weakness of the British Pound. Here’s the 15-year chart of GLEN. Commodities, like semiconductors, are cyclical.

Historical perspective on the S&P

When S&P futures debuted on the CME in 1982 the S&P was ~110. (It is now ~7,500). A 1-point change was worth $500 per contract. In 1997, with the S&P nearing 1,000 the contract was changed so that a 1-point move was worth $250 and the e-mini contract was introduced with a 1-point change worth $50. The success of the emini caused the CME to terminate the full-sized contract in 2021. The micro-emini S&P contract was introduced in 2019, with a 1-point change worth $5, which is 1/100th of the origional value of a 1-point change as the S&P soared by ~70X over the past 44 years.

Interest rates

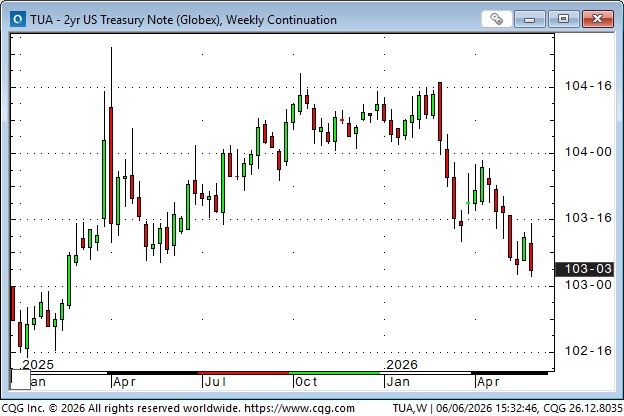

Friday’s NFP report was much stronger than expected and “cemented” the notion that the Fed will not be cutting interest rates this year, and will likely raise rates by at least 25 bps before yearend.

The 2-year Treasury closed the week at a 16-month low,

While the ultra-long bond future remained well above recent lows. The yield curve has been flattening the past couple of weeks. (Maybe the long end likes the idea of the Fed raising short rates to “cool” inflation, or maybe some investors took profits in the high-flying stock market and sought safety in the bond market).

Higher US rates put a bid in the USD

The DXY US Dollar Index rallied to a 2-month high (blue ellipse) on the strong employment report (and thoughts that next week’s CPI report may be over 4%).

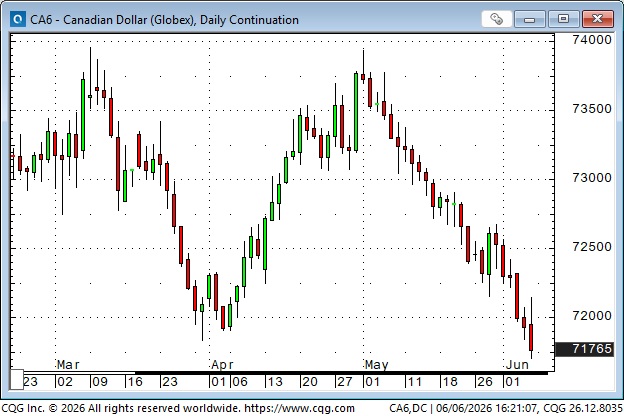

The Canadian Dollar has been in a nearly relentless decline for the past 5 weeks as the USD has risen against most currencies and as interest rate differentials between Canada and the USA have widen in favor of the USA. This week’s CAD close was the lowest since November 2025.

Higher US rates and a higher USD – toxic for gold

The Comex front-month gold futures contract (currently August) had its lowest weekly close this week since December 2025, down ~$1,250 (~22%) from January’s record highs.

The precious metals have been in a speculative liquidation phase since the spike highs in January, and lower price drive more liquidation from the FOMO buyers who chased the market higher from late August 2025 to the January peak.

Energy

Nymex front-month Brent rallied ~$9 from last week’s lows Monday to Wednesday, but gave most of that back on Thursday/Friday.

Grain markets

Grain prices perked up this spring on fears of fertilizer shortages due to the closure of the Strait of Hormuz, but that doesn’t appear to be a significant concern now.

My stort-term trading

I started this week long CAD and short WTI – positions I established near the end of last week – and long a legacy position in Yen calls.

I covered the long CAD for a 25 tick loss on Monday when there was no follow-through to last weeks rally.

I covered the long WTI position for an $8 gain on Thursday when prices turned lower after a stiff 3-day rally.

The long Yen calls expired worthless on Friday.

I shorted the S&P on Tuesday and covered for a decent gain in the Wednesday overnight market after prices fell ~80 points during the Wednesday day session. I was glad to have covered when the market rallied back on Thursday, but I missed the big plunge on Friday. I was flat going into the weekend.

Thoughts on trading

I subscribe to several Substacks and make trading comments when something catches my attention. You can read those comments (free of charge) here: (32) Victor Adair | Substack

On my radar

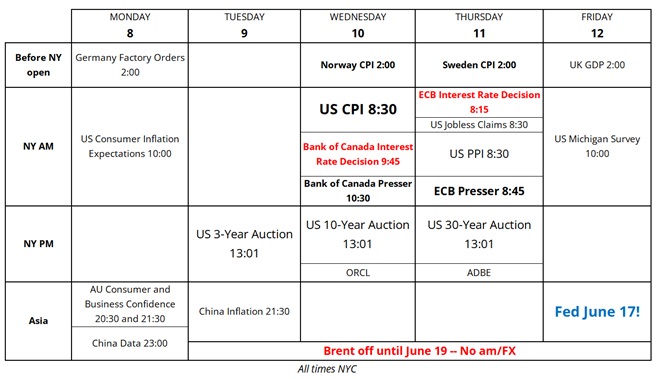

Here’s a calendar from Brent Donnelly for the week ahead.

No Trading Desk Notes next week

I plan to be in Vancouver late next week to participate in a fund-raising golf tournament for Special Olympics and to attend a Celebration of Life for one of my best friends over the last 50 years.

The Barney report

One of Barney’s favourite places to go for a walk (run, chase the ball, meet other dogs and people) is an open field of ~20 acres that is mostly surrounded by forest. This time of year, the grass is getting tall and when I try to hide from him (we always play hide and seek) he always delights in finding me. (Papa, you’re not very good at hiding!)

Listen to Mike Campbell and me discuss markets

In this morning’s Moneytalks show Mike and I discussed the sharp fall in the stock markets yesterday, and some of the reasons for the fall. We also chatted about the Glencore IPO in 2011 which turned out to be great for Glencore and not-so-great for investors. You can listen to the entire show here. My spot with Mike starts around the 1-hour and 4-minute mark. I recommend listening to the entire show. My friends Kevin Muir and Andrew Ruhland were also interviewed by Mike this week.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.