Global stocks surge higher as Iran war escalation risks fall

At the end of March, the S&P was down ~10.5% from January’s record highs (blue ellipse), but has since rallied over 7% as the market priced in a reduced risk of escalation in the Iran war. Notably, the market began to rally five days before Trump’s latest escalation deadline, set for Tuesday, April 7.

The S&P had fallen for five consecutive weeks since the start of the war before reversing higher. This week’s rally was the biggest weekly gain since the recovery from Liberation Day in April 2025.

The initial rally off the lows looked like aggressive short-covering after five weeks of decline, with the 2nd leg higher spurred by the announcement of a “ceasefire” (blue ellipse) shortly before Trump’s Tuesday deadline.

The reversal in the S&P at the end of March, as the Iran war raged, looks similar to the March 2020 reversal, when the market had tumbled ~35% in 6 weeks amid covid fears.

The NAZ, the Trannies, and the Russell 2000 all traded this week above their levels before the war started, and the Trannies hit all-time highs. The S&P and the DJIA are still below their end-of-February pre-war levels, but they are back above their 200 DMA.

CAT is also at an all-time high, up nearly 200% in the last 12 months. (Power generation trumps Middle East wars).

The high-flying energy sector stocks have reversed.

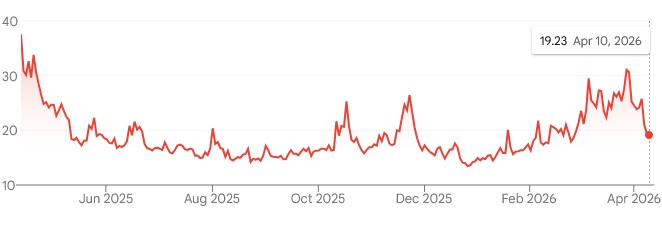

Volatility across markets has dropped sharply. The Vix hit 31% in late March, but ended the week at ~19%.

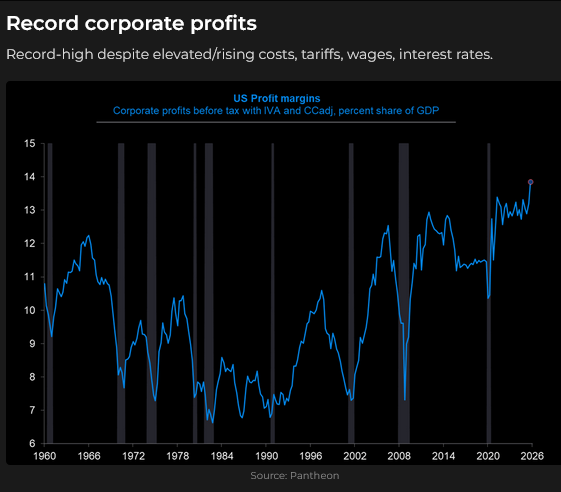

Earnings drive share prices.

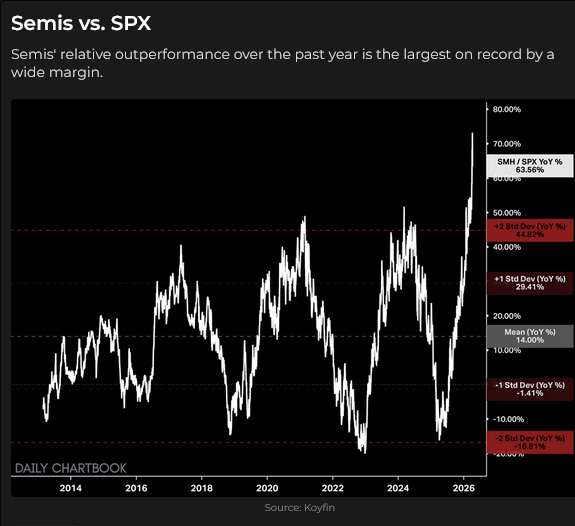

Semis are smoking hot.

Software, not so much.

The Toronto index reached record highs on the first day of the Iran war, sold off for three weeks, then turned higher before the S&P, and has closed green for the past three weeks.

The Nikkei was at an all-time high at the end of February (up ~100% from the Liberation Day lows), but fell ~17% to the late March lows, before bouncing back sharply with other global indices.

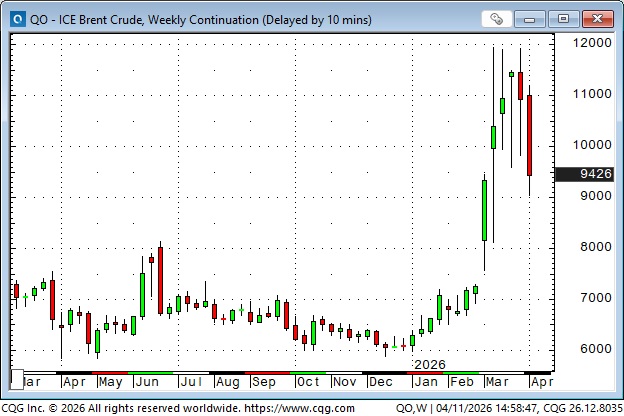

Front-month ICE Brent futures traded as low as $60 in January, soared ~100% to ~$120 in March, but have closed lower the past two weeks.

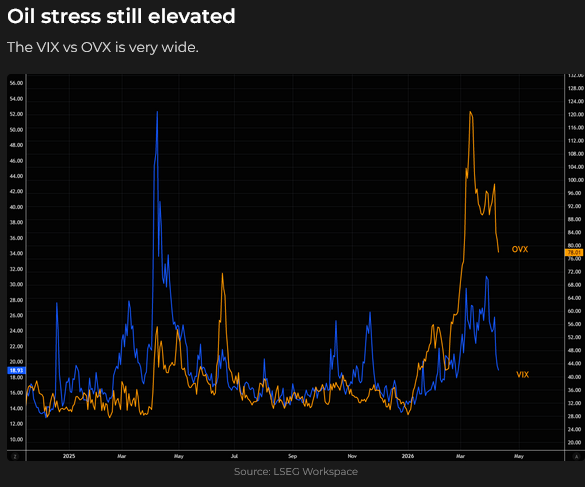

Oil volatility has fallen, as VOL across assets has dropped, but it remains historically high.

The stock market has rallied back from its lows much more than crude oil has fallen from its highs. The “acid test” for crude prices is whether physical oil is coming out of the Hormuz Strait.

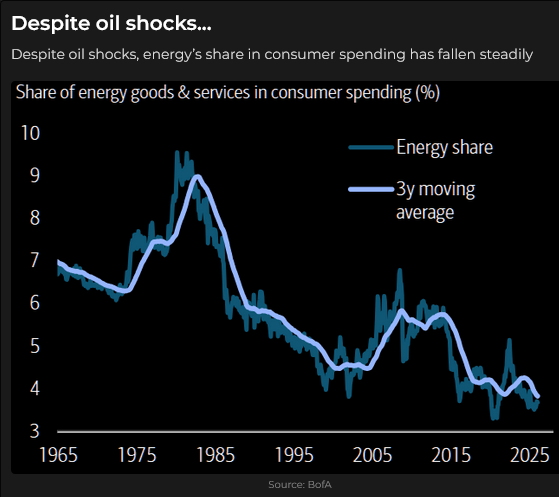

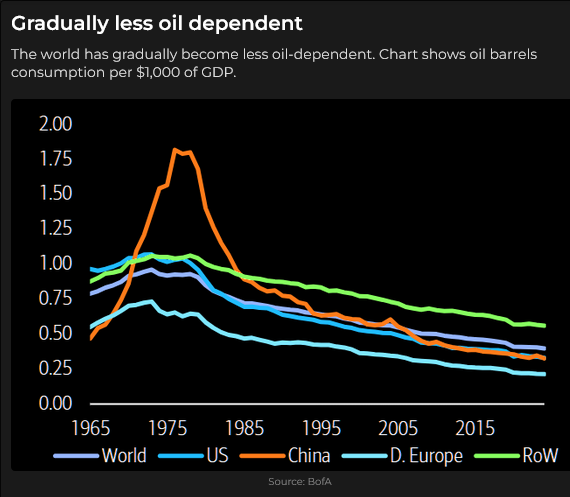

In some respects, at the March lows, the stock market had “over-discounted” the effects of higher crude prices in the Middle East on the American economy (the US is a net exporter of oil/natural gas).

And perhaps on the rest of the world as well.

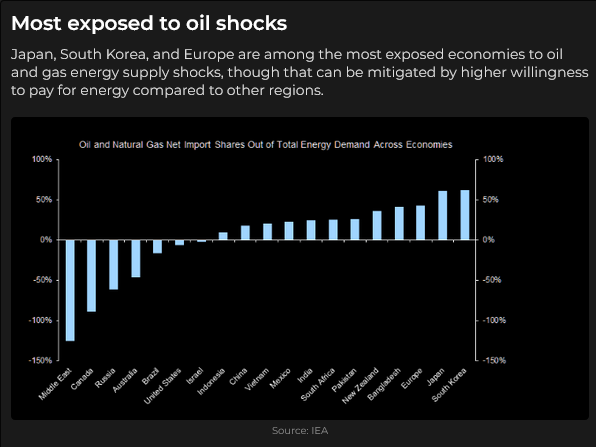

Obviously, some countries are more exposed to oil shocks than others (Europe, Japan, South Korea and New Zealand come to mind), but I was puzzled to see Australia being less exposed than the USA on this chart from the IEA. Perhaps it’s because Australia is a major LNG exporter.

Currencies

The DXY US Dollar index fell to a 4-year low in late January (when Trump said he was not concerned by the weak USD). It bounced back ~2% in February, but the market was still heavily short the USD when the Iran war started at the beginning of March. The USDX rally in March was driven in part by a “flight to safety” but also by traders unwinding short USD positions. The weakness in the USDX over the last two weeks may have been caused by the unwinding of “flight to safety” trades.

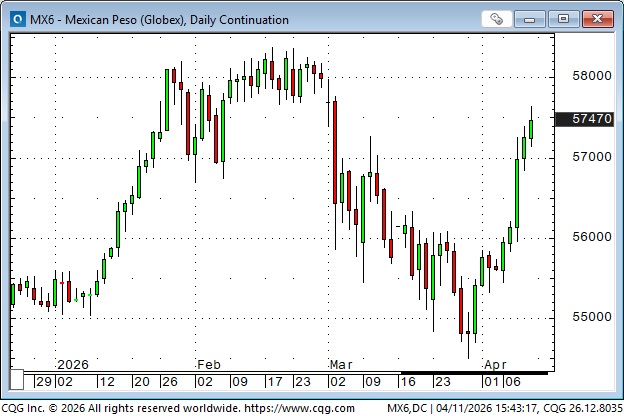

The Mexican Peso fell to 3-year lows in February 2025 on Trump’s tariff bluster, then rallied ~25% to February 2026 (think “carry trade” with Mexican short rates substantially higher than US rates). The Peso fell ~7% in March as the Iran war raged, but reversed sharply from the end of March as cross-market sentiment swung to a possible de-escalation.

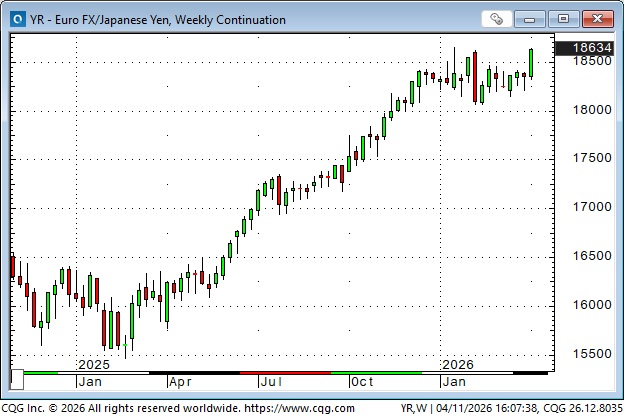

The Japanese Yen traded lower in early March as most currencies fell against the USD, but fears of intervention restrained the fall. The Yen rallied mid-month on PM Takaichi’s visit to the White House (blue ellipse), but fell back again into the month-end. Over the last two weeks, the Yen has been the weakest of the G10 currencies against the USD.

The Euro has been much stronger than the Yen over the past two weeks, driving the Euro/Yen spread to a record high.

Gold

Gold rallied to near record highs on March 2, the first day of the Iran war, but heavy (margin call?) selling took the market down nearly $1,400 to the March 23 lows. Gold bounced back and likely benefited from a weaker USD and falling interest rates over the past two weeks. Despite the wicked day-to-day volatility in gold YTD, it is ~$1,800 above where it was a year ago today.

Interest rates

Interest rates rose sharply during the first three weeks of the war as surging oil prices had traders worried about higher inflation. Interestingly, both short and long rates stopped rising after three weeks and began to trend lower, before global stock markets reversed their decline and began to rally.

Trump is scheduled to travel to China on May 14 to meet Xi.

Thoughts on trading

I’ve done very little trading since the Iran war started because I’ve been concerned that violent price moves might result in losses much larger than I’m willing to take. Risk management takes priority over everything else in my trading. When VOL skyrockets, I back away.

It’s been useful for me to practice patience, given the deluge of “fake news” and wild price action across the markets I typically trade. My trading account balance is modestly bigger than it was at the end of February, and I’ve had plenty of time to reflect on how and why I trade the way I do.

My short-term trading

I started this week flat, with no positions, with markets dead in the water on Easter Monday ahead of Trump’s Tuesday evening “Deadline.” I could easily imagine that a severe escalation against Iran would cause it to lash out at other Persian Gulf countries, resulting in “Mutually Assured Destruction,” especially if both sides targeted water desalination facilities.

I welcomed the last-minute agreement for a two-week ceasefire (some folks said Xi Jinping told Iran to agree to a ceasefire, and that’s plausible given that Persian Gulf oil represents ~40% of Chinese oil imports, and in a post-escalation world, there might have been very little oil available). I didn’t want to chase the rallies in the stock indices or (most) currencies, so I just waited.

I shorted the Yen when its rally faded and held that position into the weekend.

Wrap

I’ve no idea what will happen in the Islamabad talks, but I’m hoping markets will “settle down” and I can get back to trading more actively.

EDIT: Just moments after I posted this, Vance said they did not reach an agreement and that the US delegation would go home. My guess is the market will not like this news, and we will see a reversal of this week’s price action when markets reopen on Sunday afternoon.

The Barney report

Barney and I are enjoying the warmer spring weather as we walk the forest trails. One of our favourite walking places has lots of mountain bike trails that are “signed” by their creators. Here’s Barney checking out a trail sign.

Here’s Barney watching the Masters on Sunday morning.

Listen to Mike Campbell and me discuss markets

On the latest Moneytalks show, Mike and I reviewed the wild moves across markets over the last five weeks, especially since the ceasefire. You can listen to the entire show here. My spot with Mike starts around the 50-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.