A vicious circle of aggressive selling, thin liquidity, volatility and fear

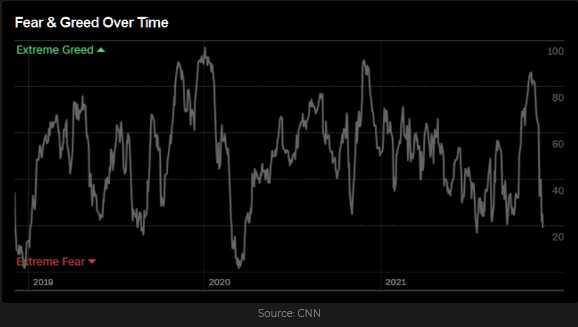

Given the drama since Thanksgiving Friday, it’s hard to believe that the leading North American stock indices were at All-Time Highs Monday of last week. It’s also hard to believe that, with the DJIA, S+P, NAZ, TSE and VTI indices down only ~6% on average, implied volatility has doubled, and the fear/greed index has plunged to levels not seen since March 2020.

This year, a tidal wave of retail money has flowed into the stock market. Market risk has increased because of all that extra “new” money

More than half of that money has gone into passive, index-linked investments – boosting the value of those indices – and especially the value of the handful of large-cap stocks which dominate those indices.

Passive investors expect “small corrections,” but they plan to “stay the course” because, inevitably, stocks only go up. I don’t expect any significant selling from that sector – unless the indices remain in a bear trend for six months or more. If those folks ever start selling, we will see what a real bear market looks like! (Who will take the other side of that trade?)

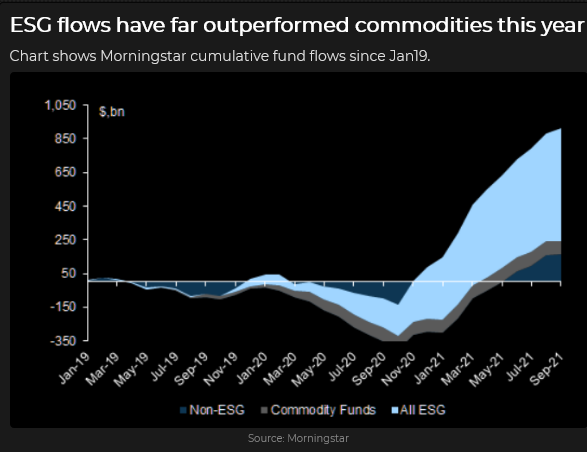

Other retail money has gone into “active” investments – everything from niche hedge funds (especially anything with ESG in the name) to YOLO kids buying deep OTM options. Some of that money has been Buying the Dip since last Friday (ouch), but I bet you some hedge funds/ CTAs have sensed trouble ahead and are hitting the bid to lock in a good performance record for 2021.

Regardless of who has been doing what, the short-term price action has been very choppy (up or down the equivalent of 500 Dow points in less than an hour a few times this week), and the trend has been down. Volume has been relatively high, sentiment across asset classes has taken no prisoners.

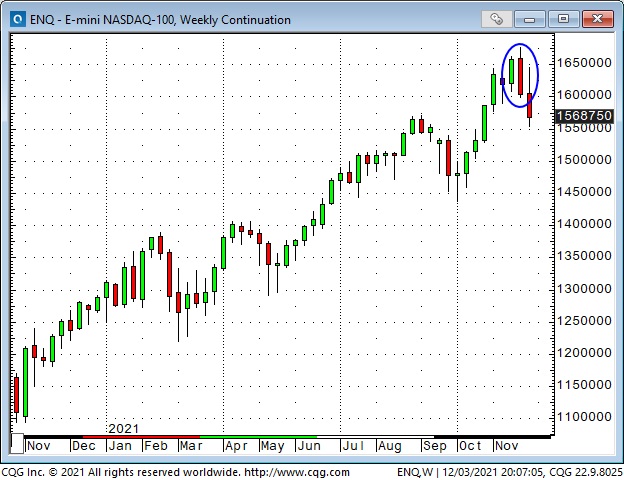

Last week, the S+P and NAZ charts registered a Bearish Weekly Key Reversal Down from All-Time Highs.

Bonds have soared as stocks and commodities have tanked

The TLT (20+ year maturity) and the Ultra-long T-Bond futures contract (25+ year maturity) closed the week at their highest prices YTD. If the bond markets were worried sick about inflation, that wouldn’t be happening – so this must be a fear-induced bid, given that the short end is pricing in at least two Fed interest rate increases next year. The ULA is up 11 points from last Friday’s low – the biggest/fastest increase since the Covid ramp in February 2020.

The US Dollar Index had its highest weekly close in 16 months

When market sentiment gets fearful, the USD gets bid. The following currencies closed this week at their lowest YTD levels: GBP, CAD, AUD, NZD, NOR, SWE, IND, and, of course, Turkey. Many other currencies are very close to their lowest levels in (at least) a year. (Notable exceptions, Israel, China.)

The Canadian Dollar has closed lower for seven consecutive weeks, as has the Goldman Sachs Commodity Index. (WTI has closed lower for six straight weeks.) The CAD had a brief rally this Friday on the much-stronger-than-expected employment report, but as stocks and crude fell and the USD rose, the CAD reversed to close on its lows.

Gold rallied ~$120 on the “inflation” story in early November – but gave it all back the last two weeks

The Open interest on Comex gold futures shows speculators chased the gold price higher and then bailed out as the price fell back to month-ago levels.

Silver tumbled as much as $3.50 (14%) from mid-November highs, with Comex open interest falling to near 8-year lows.

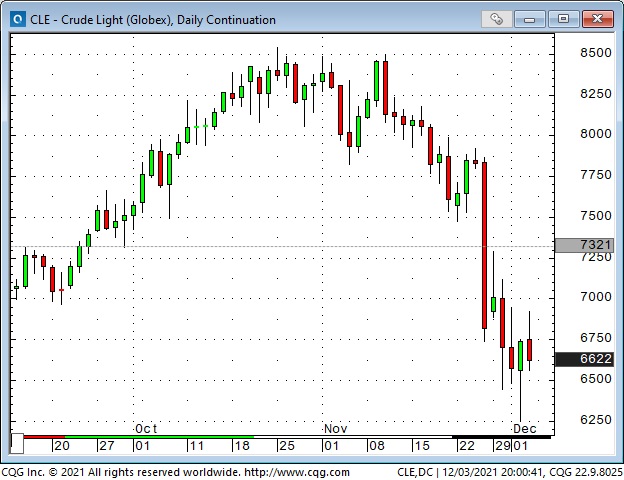

WTI crude oil dropped 27% from a 7-year high of ~$85 to ~$62

Front-month WTI tumbled more than $11 on Black Friday. The HUGE premium of front-month WTI over the deferred months evaporated. OPEC+ went ahead with their scheduled increase of 400,000BPD.

My Short-Term Trading

In the On MY Radar section of last week’s Notes, I said that I didn’t know if Black Friday’s dramatic (Omicron inspired?) plunge in ultra-thin liquidity conditions was the start of “something” or just a flash-in-the-pan – but I was leaning towards “something.“

Stock index futures and WTI opened sharply higher Sunday afternoon (Omicron wasn’t so bad after all.) Stock indices took out Friday’s day session highs before the opening of the Monday day session. Friday’s nose-dive looked like a flash-in-the-pan, so I bought the Dow and the CAD.

Those positions were stopped for small losses Tuesday morning when Powell kissed “transitory” goodbye.

Over the next few days, I traded the S+P and the CAD, looking for a bounce. I bought futures and sold OTM S+P puts with a 30 vol. Every trade initially worked in my favour. I made some money and lost some money, but my P+L was down ~0.50% on the week.

I was flat going into the weekend – ruefully wondering how I missed making money on the short side.

On My Radar

If I think in terms of a multi-month time frame, my bias is to believe that the “chasing” of risk assets is WAY overdue for a correction. In terms of a day-to-day time frame, I think we’ve had a pretty good correction over the past two weeks.

I try to avoid taking a position based on a “story” (for instance, copper has to go a lot higher because of global electrification and a shortage of new mine supply.) I understand that many successful traders have made fortunes because they bet big and were right on a story. (The Big Short.)

You don’t hear about all the people who believed a story, bet big, and went down with the ship because they knew they “had to give it a little more time.”

Stories are seductive, and maybe you have to believe in something to make money from trading/investing. Or perhaps you have to believe in yourself and your method.

Last week, I referenced a clip of the Peter Brandt interview with (Market Wizards) Jack Schwager. I watched the full interview on RTV this week. Jack said that the 70 very successful traders he featured in his books seemed to have no personality or educational traits in common but that they all had found a way to participate in markets that suited them. They all had a great appreciation of risk management/control – to the degree that their long-term success depended more upon risk management than upon their methodology.

Jack succinctly said that the Wizards had “no loyalty to a position.” I took that to mean that they did not believe in stories.

Some folks would argue that you need some degree of “belief” in a trade to be able to stick with it during a short-term setback (however you define “short-term setback.“) I would counter by saying that I would stay with a trade until my trailing stop was hit.

I believe that every person has to find their own way to trade/invest – that successful traders have found a unique way to trade that suits their personality, time frame, and risk tolerance.

Thoughts On Trading

Reminiscences of a Stock Operator has been my bedtime reading lately. I bought my first copy of that book over 40 years ago, and I’ve re-read it every couple of years since. It was written ~100 years ago, but it still rings true today. It’s the story of a man finding his way to successful trading through trial and error. His style is probably WAY too aggressive for most people (including me), but his observations of himself, the people around him, and the markets make it a good read. I recommend it to you.

Quotes From The Notebook

“I don’t believe in much, but I sure do believe in reversion to the mean.” James Clarke, Successful Options Trader, 2019

My comment: Back in the 1980s, Jimmy worked for a prop trading firm in an office with no name of the door, 19 floors above the CBOE. He described his trading methodology as “being the buyer of last resort for OTM S+P options.” We were having dinner in 2019 – the first time we had seen each other in several years – and the subject of “what do you believe in” came up.

“Anything that will generate yield is being monetized.” Diego Parrilla, 2016

My comment: I had been impressed with the book Diego Parrilla, and Daniel Lacalle wrote – The Energy World Is Flat. This quote is from a subsequent interview. One of my “opinions” back then was that option volatility was WAY lower than it “should be” because people were selling vol to generate yield – that reaching for yield had become the most crowded trade in the world.

The lust for yield has overwhelmed Prudence. Bob Hoye, 2017

My comment: My friend Bob Hoye has been a treasure trove of quotes, and this one ties in beautifully with Diego’s selection.

A Small Request

If you like reading the Trading Desk Notes, please do me a favour and forward a copy or a link to a friend. Also, I genuinely welcome your comments. Please let me know if there is something you would like to see included in the TD Notes. Thanks, Victor

Barney: (13 weeks old, 20 pounds) Yeah, hit that bid before it disappears!

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Therefore, this blog, and everything else on this website, is not intended to be investment advice for anyone about anything.