Will markets get “back to business” with a BANG after Labor Day, Sept 5th?

We are in the “silly summer season,” and the “adults” are away. Trading volumes are light, but my veteran trader’s intuition tells me that markets may get “back to business” with a BANG once we get past Labor Day.

September will bring “winter” into focus – especially concerning soaring European energy prices and all that implies for Europe (and elsewhere: North American Natgas has traded at 14-year highs on European LNG demand.)

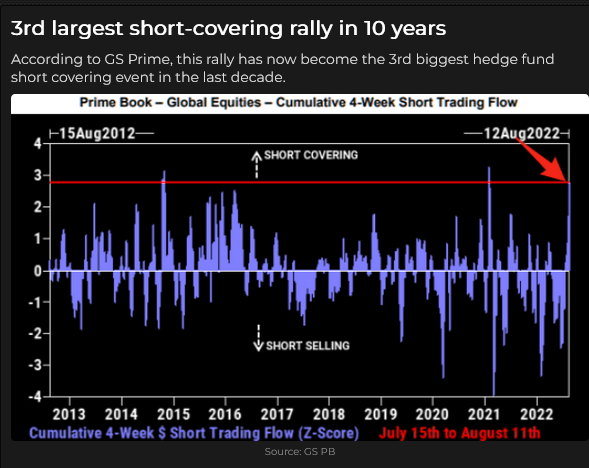

Stock indices have been in a bear market rally since the 20-month lows made in mid-June. The S+P has rallied ~19% from the June lows to this week’s highs, but 30% of that rally is attributable to just four stocks: AAPL, MSFT, AMAZ and TSLA.

The S+P kissed the primary downtrend line from the January All-Time Highs and the 200-day MA this week and fell back as the hardcore bears predicted a coming disaster.

The rally was fuelled by short-covering (remember the DJIA dropped ~3,000 points over seven days ahead of the June FOMC meeting), FOMO (Money managers have to chase this rally after a miserable first-half performance), corporate buybacks and retail buying.

The US Dollar Index hit a 20-year high in July and fell back ~4% into mid-August, but for the last 7 trading days, it has been rising against virtually all currencies.

The Euro is just above Par with the USD (it hasn’t been below Par for 20 years.) The Euro/Swiss is at All-Time Lows (down 9 of the last 10 weeks – down an astonishing 9% in just over 2 months – the spread is a terrific metric for the Eurozone existential crisis.)

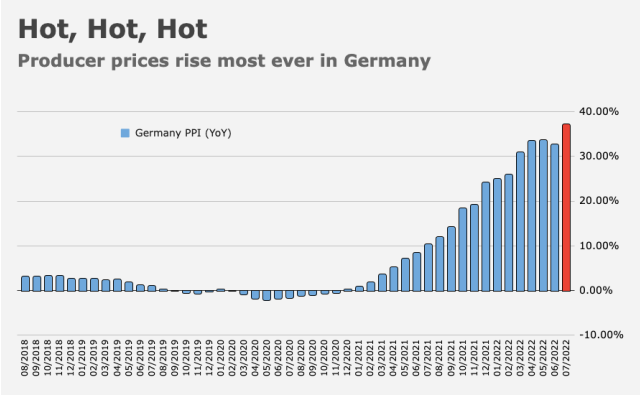

Soaring energy prices are stressing German manufacturers.

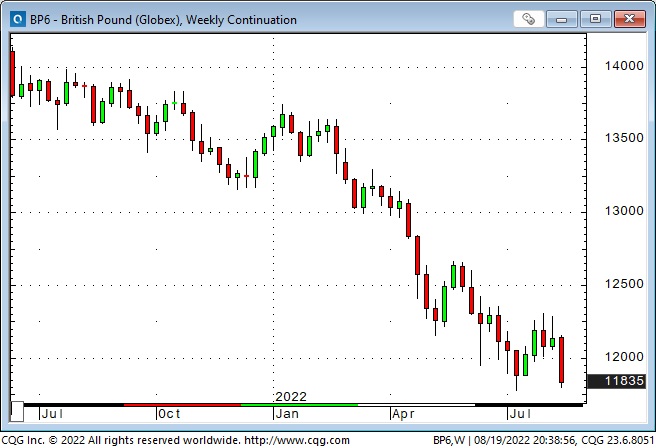

The British Pound has been in a steady downtrend against the USD for the last year.

The Yen has dropped ~25% against the USD since January 2021 and hit 24-year lows last month.

The Chinese Renminbi fell hard this week after the PBoC CUT interest rates to counter slow economic growth (think covid lockdowns, deleveraging real estate, etc.) In this chart, a rising price denotes more RMB needed to buy a USD.

My FX trading mantra for 40+ years has been that capital flows to the USD for safety and opportunity. We could see that “flow” accelerated this fall if the market gets in a “risk-off” mood.

US Interest rates have been rising for the past 12 months. The 2-year Treasury yield is near 14-year highs ~3.25%. Compare that to 2-year yields in Germany at ~0.7%, Japan at minus 0.9%, the UK at ~2.5%, and Mexico at ~9.5%. The US 10-year yield is just under 3%.

The minutes of the last FOMC meeting (July 26/27) were released Wednesday, and they, along with day-to-day comments by Fed officials, seem to indicate that the Fed is determined to curb inflation and inflation expectations – they are NOT contemplating backing away from their aggressive policies – even if those policies create a recession. This coming week (August 25/26) will be the annual Jackson Hole event.

The Goldman Sachs Commodity Index (with a heavy energy weighting) hit a 14-year high following the Russian invasion – creating a spectacular 3.7X rally off the 20-year lows made following the Covid Panic in March 2020. The index dipped a bit into April, rallied back to make a lower high in early June, but slid lower for seven consecutive weeks and has gone sideways at these lower levels for the past six weeks.

Gold made All-Time Highs ~$2,080 following the Russian invasion but dropped ~$400 to 15-month lows in July – pressured by rising interest rates and a strong USD. Gold rallied as much as $120 from the July lows (as the USDX slipped from 20-year highs), but this week gold dropped ~$50 as the USD stormed back. The declining open interest in COMEX gold, net gold ETF sales this year and a ~40% slide in GDX since April (the gold miners ETF) point to a “lack of interest” in gold over the last several months.

Front-month WTI Crude oil traded below $86 this week for the first time since January. At this week’s lows, the market was down ~$38 (30%) from the June highs and down ~$44 (34%) from the Russian invasion highs.

Backwardation (the price premium of front-month contracts over deferred contracts) has collapsed sharply, with the Sept/Dec spread falling from $9 to $1 in the last month. Steep backwardation is usually understood to mean strong demand for immediate delivery, and falling backwardation implies that demand for quick delivery is fading.

Open interest (but not volume) throughout the fossil fuel futures markets has fallen to multi-year lows – perhaps the wicked price volatility has caused traders to reduce the size of their overnight positions. (The grain markets and stock indices also have had nasty price volatility and reduced open interest.)

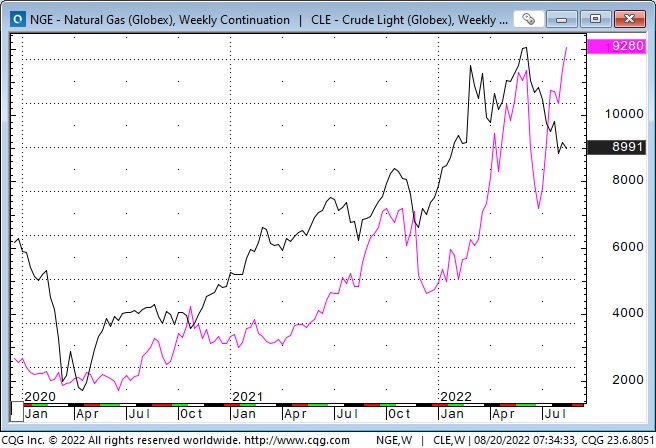

WTI prices and Natgas prices moved up and down (more or less) together since the Covid Panic in early 2020 – but for the past two months, Natgas (pink line) has soared as WTI fell.

My short-term trading

I started this week short CAD, Euro and Yen – positions I established late last week. I was stopped out of the Yen on Monday (within a few ticks of the day’s high) for a slight loss. (I had lowered stops on all three positions to around breakeven levels after the markets closed lower last Friday.)

I took decent profits on both the CAD and the Euro on Monday and was happy to have done so when they bounced back on Tuesday.

The problem was that all three currencies continued lower from Wednesday to Friday (the Yen fell 260 points after my stop was hit), and I could not find a spot to re-establish my short positions!

Another “problem” was that getting short the stock indices was “On My Radar” for this week. I was slow to act but finally got short near the low of the day on Wednesday – a small position with a tight stop. I was quickly stopped out for a slight loss and never got back short as the market closed lower on the week.

I was flat at the end of the week, with decent net profits, but my “feeling” was that I had left WAY too much money on the table!

Analyzing my short-term trading

One of my favourite “sayings” is that it is essential to keep the time frame of my trading in sync with the time frame of my analysis, and I haven’t been good at that lately.

I have had some good “ideas” about possible market moves, but perhaps due to the wicked short-term price volatility across many markets, I have been trading with stops that have proved too tight. For instance, I shorted gold on August 10th at $1,808 and covered the position at $1,816 later that day (it was moving to new 6-week highs – an excellent reason to cover shorts!) Gold topped out at $1,824 that day and closed this week at $1760 – which is $48 below my short entry point.

Now I’m the first guy to acknowledge that trading is never a “game of perfect” and I’m very familiar with the experience of being “early” on a trade, losing money on the trade, and then watching (like a sad puppy!) as the market goes where I thought it would, while I’m unable to pull the trigger and re-establish the trade.

I have also often been “early” on a trade, lost money but re-established the trade and came out well ahead.

This self-analysis is not whining; it’s an honest question about what changes I could make that might improve the profitability of my trading. My honest answer: My trading time frame has been too short lately relative to my analysis time frame. To “lengthen” my trading time frame to get more in sync with my analysis time frame, I will have to do two things, 1) use wider stops and 2) try to hold winning positions longer.

Quote of the week

In keeping with my frustration at leaving too much money on the table, I thought this quote from Jimmy Jude (on my friend Kevin Muir’s website) was perfect!

The Barney report

Barney was bitten by another dog when my wife took him to the dog park about ten days ago. He yelped when he was bitten, but he seemed to shake it off, but we wanted the Vet to have a look. The Vet couldn’t see him until this past Monday, and the wound was no big deal, but to be safe, the Vet gave us some antibiotics and a solution to put on the wound to prevent an infection. The bad news is we had to stay out of the ocean this week to allow the wound time to heal.

The owner of the dog that bit Barney was shocked – his dog had never bitten another dog, and he apologized profusely. The truth is that Barney has been getting more aggressive with some other dogs lately and probably deserved what he got. So (and dog owners knew this was coming), Barney is scheduled to get snipped when he turns 1-year old at the beginning of September.

Barney loves to be off-leash.

A request

If you like reading the Trading Desk Notes, please forward a copy or a link to a friend. Also, I genuinely welcome your comments, and please let me know if you’d like to see something new in the TD Notes.

Listen to Victor talk about markets

I’ve had a regular weekly spot on Mike Campbell’s extremely popular Moneytalks show for >22 years. The August 20 podcast is available at: https://mikesmoneytalks.ca.

I did my regular 30-minute monthly interview with Howe Street Radio on August 5th. I talked about my Pelosi/Taiwan trade, the employment report, currencies, energy, gold, the Canadian dollar, my Macro views and what I think is “the most important thing” impacting all those markets. You can listen here or here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.