Too much leverage?

You can’t have a bubble without leverage, and making the bubble bigger requires even more leverage. At some point, too much leverage sets the stage for a meaningful correction. If we’re not there already, we’re close.

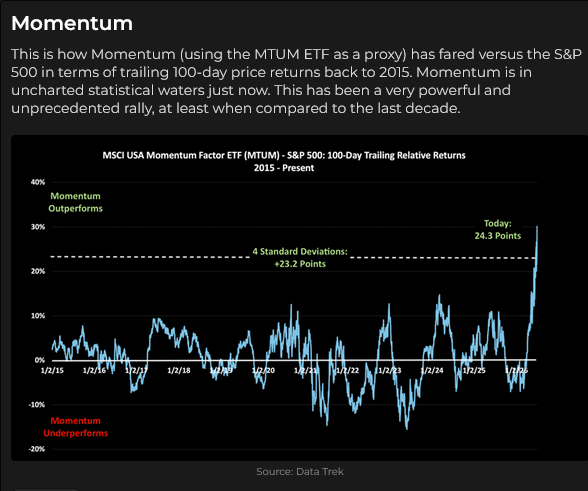

In last week’s TD Notes, I wrote, “the biggest knowable (non-black-swan) risk may be overleveraged positioning. This chart accompanied that:

FINRA reports that US margin debt was ~$1.42 trillion at the end of May 2026, up ~54% YoY. (The end of June report will be available in 3-4 weeks; I expect it will be a bigger number.) Borrowing costs are rising.

Veteran traders know that there are multiple ways to add leverage. Still, you don’t need to make a list when you see the “wild and crazy” price action we’re seeing recently in the equity markets – you know there’s too much leverage, just like you knew there was WAY too much speculative leverage in gold and silver in December and January.

The S&P has traded broadly sideways near record highs over the last 9 weeks, after rallying ~18% from the late-March lows.

The Nasdaq has a similar pattern, up ~34% from the March lows to the early June highs.

The DJIA closed Thursday at a record high, up ~18% from the March lows.

The TSE had a record-high weekly close, up ~13% from the March lows (Canadian banks are up ~30%).

Korea was up ~80% from the March lows at last week’s highs.

Japan was up ~40% from the March lows at the June 22 highs.

The Euro Stoxx 50 Index was up ~20% from the March lows at this week’s record high close.

Earnings, earnings growth, and the anticipation of even greater earnings to come have fuelled stock market rallies. US Q2 earnings reports will start arriving in mid-July, and most S&P-listed companies will report by mid-August.

Momentum, capital inflows, FOMO, and increasing leverage have accelerated the equity market rallies.

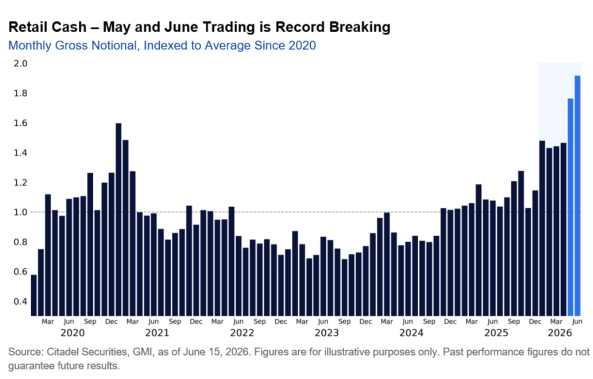

Retail is increasingly a bigger factor.

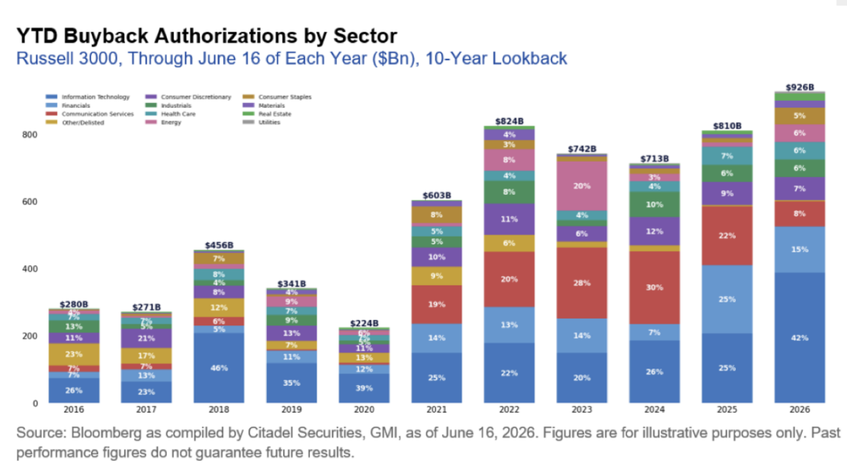

Buybacks remain an important driver of share prices.

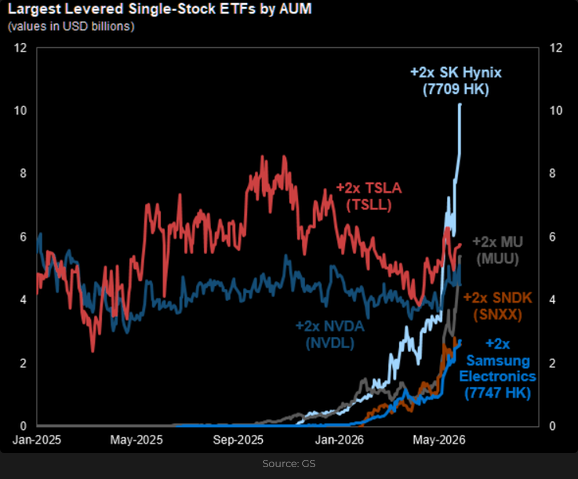

There are leveraged ETFs (which have seen massive capital inflows YTD), and then there are leveraged single-stock ETFs.

Leveraged ETFs are “great” when the underlying share price is rising, but the losses ramp up quickly when the share price is falling.

There has been wicked short-term price volatility and rotation in individual stocks, sectors, and the indices, as traders/investors have 2nd thoughts about what works, what pays, who wins, and who loses.

Currencies

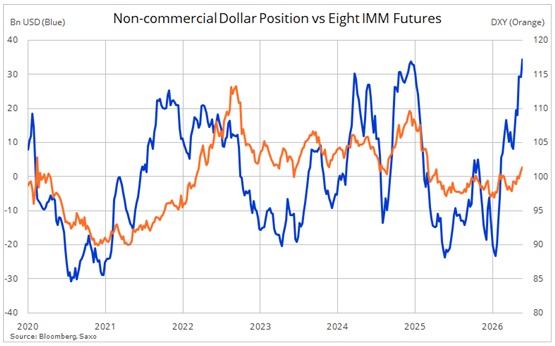

Slightly softer-than-expected employment data this week (and WTI down to ~$68) have dampened expectations of Fed interest rate hikes this year, but markets are still pricing more than one hike by year-end. Interest rate differentials remain a significant factor across FX markets. Net bullish USD speculative positioning in currency futures has risen to a multi-year high as the DXY US Dollar Index has risen from January’s 4-year lows.

The Canadian Dollar remains near 15-month lows (7050), as historically wide short-term interest-rate differentials (~140 bps) favour the USD.

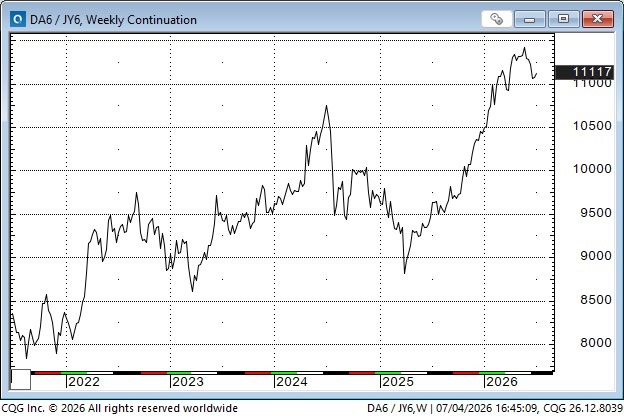

The Japanese Yen fell to 40+ year lows against the USD on Wednesday but popped higher on Thursday (blue ellipse) amid fears that the Japanese authorities might exploit thin holiday market conditions and a slightly softer USD to intervene. (Some analysts thought Thursday’s rally may have been spurred by “silent intervention.”)

Gold

Front-month August Comex gold futures dipped below $4,000 last week and again this week (down ~$1,600, or 28%, from the January record highs), but closed this week at ~$4,200.

A slightly weaker USD this week may have helped gold rally from its recent lows. There has been a relatively strong negative correlation between gold and the USDX YTD. (The blue line in this 8-month chart is an inverted DXY plotted against gold.)

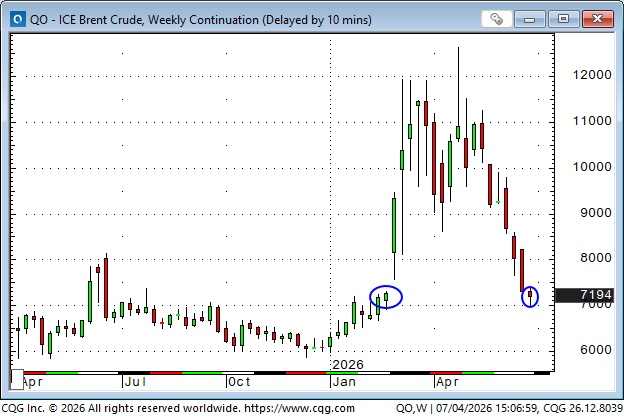

Crude oil

Front-month Nymex WTI futures have “round-tripped” since gapping higher at the start of the Iran war. Front-month ICE Brent futures closed this week slightly lower than where they closed the last week of February.

Crude oil bears (Morgan Stanley, for instance) see oil prices “steady” in the near term as global inventories rebuild, but then prices drift lower later this year as supply exceeds demand. Iran has been moving crude through the SOH but is struggling to find buyers. Crude oil bulls (Goldman Sachs, for instance) see prices higher on an inventory rebuild, then “steady” later this year.

Thoughts on trading

I only trade exchange-listed futures and options. I don’t trade individual stocks or ETFs. Within the futures and options markets, almost all of my trading is in “financial futures,” including stock indices, interest rates, currencies, metals, and energy. I don’t remember ever trading softs (coffee, cocoa, sugar, etc), and I rarely trade the Ag markets.

I think there is value in “specializing” in a few markets (you can’t do a good job at anything if you’re trying to pay attention to everything).

I pay attention to many markets that I don’t trade because I think it may help me better understand the markets I do trade. Everything is correlated to some degree. I pay close attention to correlations (especially when they break down), and I occasionally trade spreads and relative value trades. However, most of my trading is in “flat price” trades (I’m either buying or selling something).

I read a lot of research/market comment. (Sometimes I think I read too much!) I listen to and watch a lot of podcasts. I’ve read 100’s of “market” books.

I’m always looking at charts, but I’m not exclusively a “technical” trader. I subscribe to COT services to understand how traders are positioned. I have a “network” of veteran traders that I follow or exchange ideas with.

When I was younger, I was a much more aggressive trader than I am now. I’ve learned that there are old traders, and bold traders, but no old and bold traders. My expectations are more in line with achieving 40-50% annual ROI, rather than trying to grow my account 10X in a year.

I have more losing trades than winning trades. I almost always have stops “in the market” on my positions, but I will frequently exit a losing trade before it hits my stop. I have very little patience with underwater trades.

In previous Notes, I have frequently recommended Stephen Innes, a Canadian veteran trader who lives in Thailand. I’m astonished at the volume, breadth, and quality of his market comment. You can find him on Substack. Here are some links to pieces he has recently written about trading – not about markets – that I believe will be useful to any trader:

https://substack.com/home/post/p-204046154

https://substack.com/@thedarksideoftheboom/p-201271266

https://substack.com/home/post/p-201605880

Here’s a piece in which he “retells” a Bloomberg article by Simon White on the current dangers of overleverage in the markets.

https://substack.com/home/post/p-204754403

I read/follow another veteran Canadian trader, Brent Donnelly, who currently lives in New York. I just downloaded his latest book to my Kindle and started reading it. I’ve watched Brent do podcasts with Tony Greer, Kevin Muir and Maggie Lake, and I hope to get Brent on the Moneytalks podcast within the next couple of months.

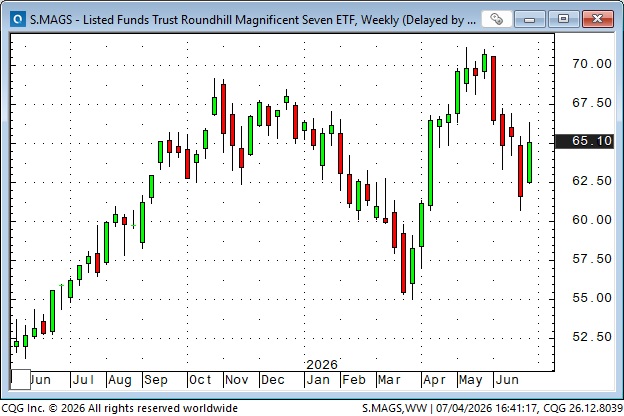

I pay attention to Mike Hartnett at BoA. His time frame is longer (much longer) than mine, but he’s had some great macro calls. He thinks the equity market is toppy here, and that if the MAGS break below $60, the broad market is in trouble.

He also thinks a break below 110 in the AUDYEN (a carry trade) would signal stock market weakness. The market traded to a multi-decade high in May. The Yen has been weak against virtually all currencies.

My friend John Johnston (JJ, Alyosha) thinks a break below 28,560 basis September on the Nasdaq would trigger a steeper decline.

My short-term trading

I started this week short the S&P, a position I established near the end of last week. I covered the trade for a tiny loss on Sunday afternoon. The market had an excellent opportunity to break down, and didn’t, so I got out. I reshorted the S&P near the highs on Wednesday (about 150 points above where I covered on Sunday) and held that trade into the weekend.

I bought the Yen on Tuesday near the day’s lows and held that trade into the weekend after it rallied briskly on Thursday amid intervention fears.

I rolled my long nat gas position into September. It has been very dull but has managed to stay above my entry price, so I still have it. If the market doesn’t rally on this heat wave, I’ll probably close it out.

I covered my long CAD early in the week for a small loss. It was a hedge against some of the FX cash market gains I’ve made in my corporate accounts over the past two months, but I decided to stay 100% long USD.

The Barney report

The first thing I do when I get up in the morning is check the markets, then I hit the shower. When I’m done in the bathroom and go back to my bedroom to get dressed, who do you think is always cozy in Papa’s bed?

Happy 250th Birthday to my American friends!

Listen to Mike Campbell and me discuss markets.

On this morning’s Moneytalks show, Mike and I discussed the equity market risks I see due to overleverage. You can listen to the entire show here. My spot with Mike starts around the 1-hour-and-9-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.