The S&P fell ~10% in March, but surged higher for the last 6 weeks, up ~17% to new record highs

The Nasdaq outperformed the S&P, rising ~28% in 6 weeks.

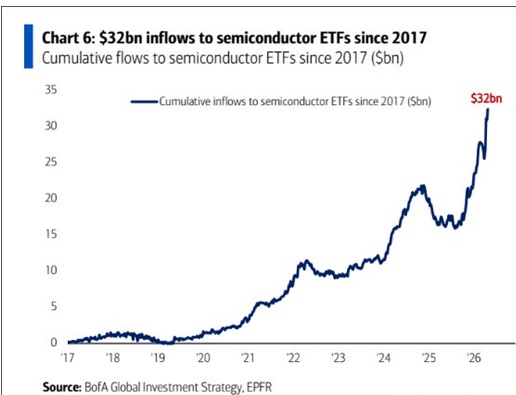

The SOXX, the semiconductor ETF, gained ~70% in 6 weeks.

North Asian markets (Taiwan, Japan and South Korea) also surged higher, with the (Korean) EWY ETF up ~65% in the last 6 weeks.

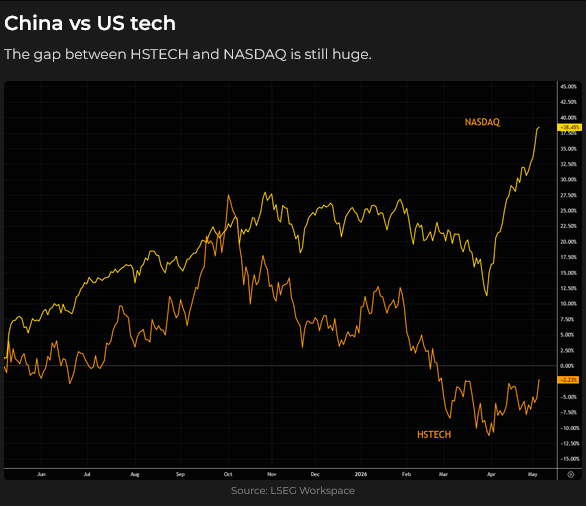

The Chinese tech index has lagged the Nasdaq and North Asian indices by a wide margin.

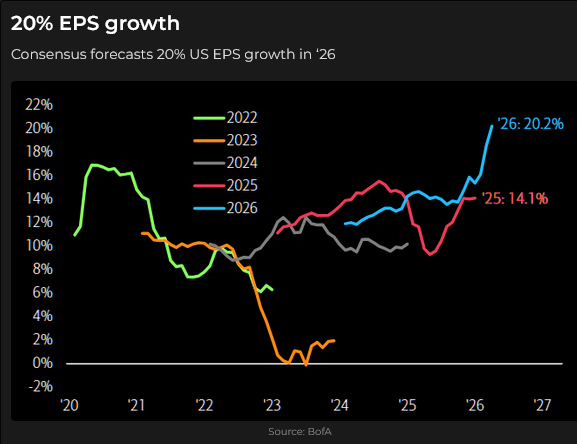

Why are stocks, especially tech stocks, rising so sharply? Part of the answer is that earnings have been strong and may remain strong.

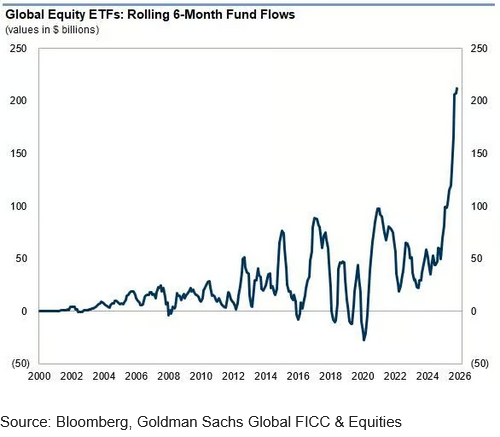

Equity markets are also rising because rising markets attract buyers.

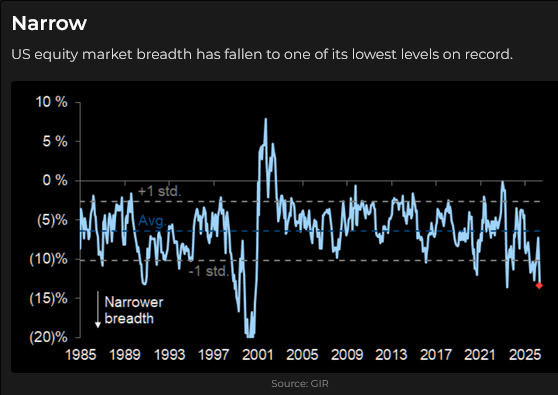

Market breadth is historically narrow, as buying is concentrated in a few big-cap stocks.

Some stocks/sectors have been “left behind” as capital has chased the tech sector.

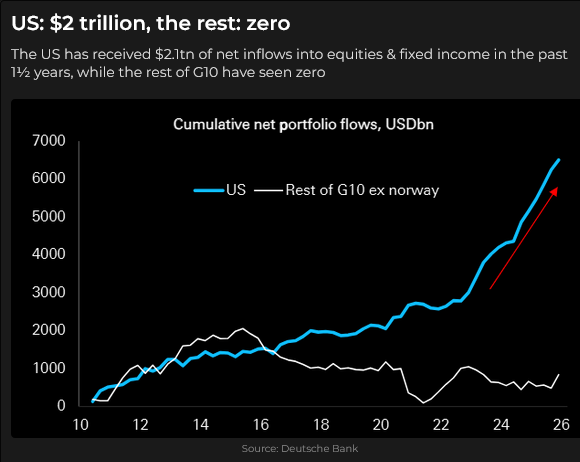

American equities and fixed income remain magnets for the majority of international capital flows.

Currencies

The DXY US Dollar Index rose ~3% in March, then turned lower at the end of the month (in sync with the equity markets turning higher) and is now back to where it was before the Iran war started.

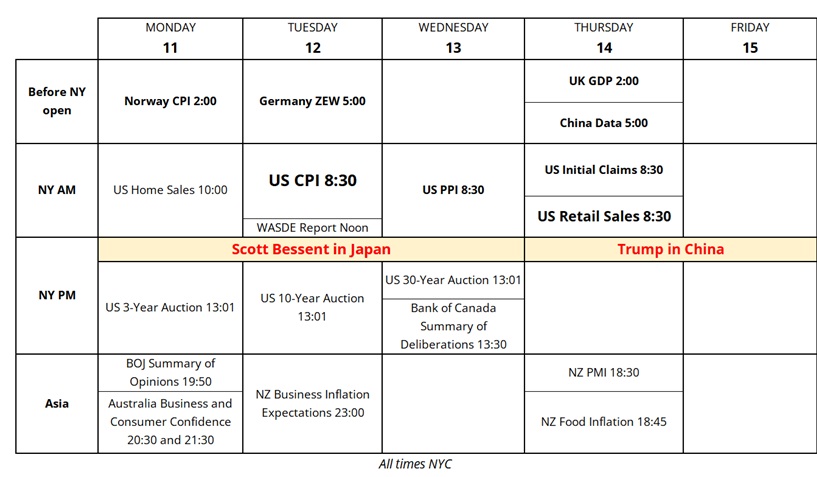

The Japanese Yen dropped ~5% from February’s highs to April’s 30+ year lows (Japan imports nearly 100% of its crude oil from the Middle East). Still, it recovered a good chunk of those losses on official intervention (blue ellipse) in late April. US Treasury Secretary Bessent will be in Japan on Tuesday and Wednesday for “talks” with Japanese officials before joining President Trump in China. There is a good chance that the weak Japanese Yen will be one of the issues discussed.

The Chinese RMB closed this week at a 3-year high, rising ~8% from the record lows reached in April 2025 when Trump and Xi were duelling with tariffs. (In this chart, a falling RMB means it takes fewer RMB to buy one USD).

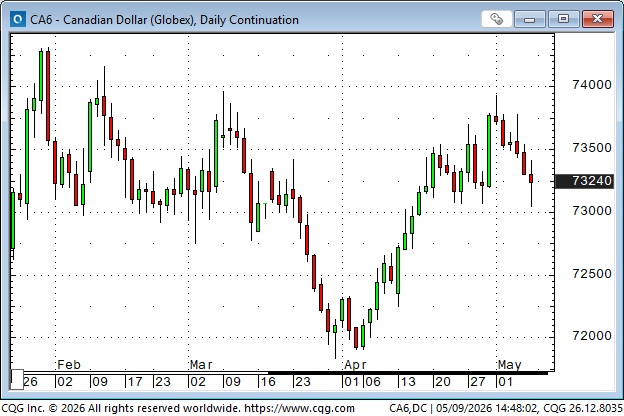

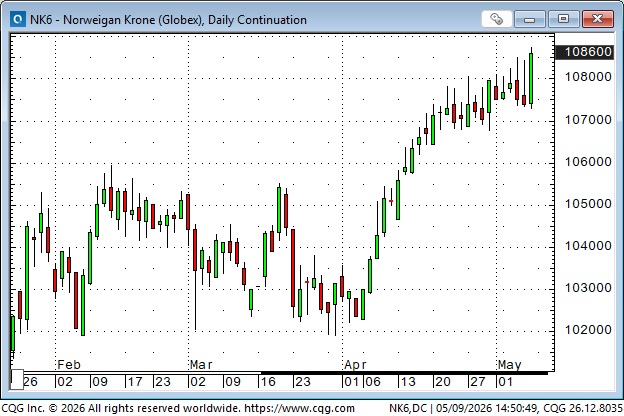

The Canadian Dollar fell with the S&P in the last three weeks of March (as the USDX rallied) and then rallied with the S&P throughout April (as the USDX fell), but it has turned lower over the last week, even as the S&P soared to new highs. It seems there is no significant “driver” of CAD sentiment and positioning (it is not being traded as a petrocurrency, like the Norwegian Krone, even though Canada exports more than twice as much crude oil as Norway).

Currency quote of the week from Mike Harnett, Chief Investment Strategist at Bank of America:

In previous TD Notes, I’ve frequently called the Euro the “Anti-Dollar”, because it is “the first place you’d go, if you want to be short the USD in the currency markets.” I’ve also said that I’d be short the Euro (and/or the GBP) on their energy policies alone, but there are other considerations, such as interest rate differentials. I’m puzzled that the EUR and GBP have “held up” as well as they have against the USD, and I have to agree with Mike Harnett: the USD’s inability to rally against the EUR and GBP is a “terrible look” for the USD.

Energy

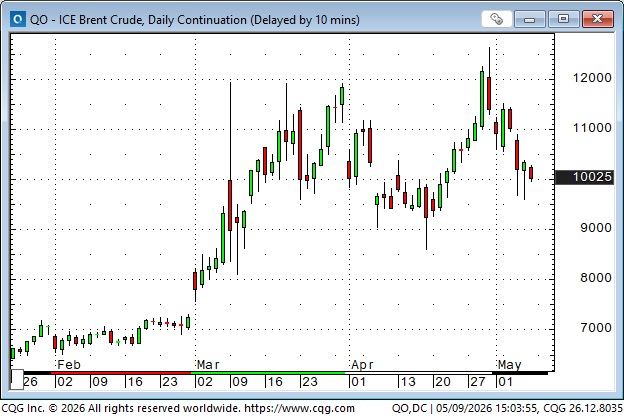

Front-month Brent crude oil futures traded above $126 last week and as low as $96 this week as the market reacts to tweets and kinetic activity between the US and Iran. While global equity markets appear unconcerned about the war/negotiations, the crude oil market is far from sanguine, especially about the impact of an extended closure of the Hormuz Strait.

Front-month Nymex natural gas futures are trading near 2-year lows, but the market has briefly traded near $1.50 in 2016, 2020 and 2024. Bullish factors for natgas include growing global demand for cleaner fuels, especially for generating electricity, the “arb” between North American and European and Asian prices, which is driving the anticipated growth in North American LNG exports, and the fact that, on an “energy equivalent” basis, natgas is very cheap relative to crude oil (which may lead to longer-term conversions, such as motor vehicle fleets converting from gasoline/diesel to natural gas). A bearish concern is that higher crude oil prices may spur a substantial increase in oil drilling, which could boost natural gas production, as it is often a byproduct of oil production.

Interest rates

Bond yields across G10 countries (X China) are higher than pre-Iran war levels. The US 30-year yield rose from ~4.6% at the end of February to a high of ~4.95% on Monday (blue ellipse).

UK bond yields hit a 36-year high this week at ~5.8%. In the UK, bond yields are set by the market, while in Japan, the BoJ controls them, keeping them artificially low (the BoJ owns more than 50% of outstanding Japanese government bonds). If the BoE kept UK bond yields artificially low by buying them, then the GBP would be near historical lows, like the Yen.

German and French bond yields are at ~15-year highs. Government fiscal policies and concerns about possible inflation from rising oil prices have pressured bond prices.

Canadian long bond yields were at 16-year highs ~3.96% on Monday’s close (blue ellipse).

Copper hit a record high weekly close

Front-month Comex copper futures hit an all-time high weekly close this week at ~$6.30.

My short-term trading

I shorted the S&P early during Monday’s session, after Friday’s weak close, and was nearly 70 points ahead on the trade by noon. But the market rallied overnight, and I was stopped for a tiny loss (I had lowered my original stop when the market moved in my favour).

I shorted the S&P again on Thursday, when it broke down from o/n highs, and was stopped for a slight loss in the o/n session.

I shorted the market again on Friday, near the day’s highs, and held the trade into the weekend.

As I wrote last week, the trend is your friend, up to a point, and the “win rate” on shorting a market that is screaming higher is less than 50%, but I like the asymmetrical risk/reward ratio if the market has a sharp correction.

I never go “all-in” on anything; I’m trading small size here, and I’m willing to take a few small losses if I think there is a “good” chance the market could break hard. I’m prepared to be dead wrong, and the impact on my P+L will be slight.

On my radar

Regular readers will know that I’ve had my eye on the Yen for months. I think that if/when it turns higher, it could be the start of a multi-year rally (after a 14-year decline!) In the Paul Tudor Jones video that I linked in last week’s Notes, he talked about waiting for a “catalytic moment” in a market.

I wonder if that moment has arrived in the Yen with the official intervention last week (and maybe more this week?) and with Bessent due to have “talks” with his Japanese counterparts this week. I understand “why” the Yen has fallen to multi-year lows (like I understand why the equity indices have soared to record highs), and “the turn” may come from lower levels, but, if there is to be a “turn,” then it will come before everything that drove the Yen lower is history.

Trump meets Xi in Beijing in a few days. Who knows what may come of that?

Here’s a calendar from Brent Donnelly for the week ahead. I think the “under the radar” event may be Bessent in Tokyo.

The Barney report

Temperatures rose to the low 20s here earlier this week, and I noticed that Barney, wearing his fur coat, was feeling the heat and kept to the shadows as much as he could while we were out for walks. I carry a litre of water and a little rubber drinking bowl to keep him hydrated.

Here he is with both paws on the kitchen island, wondering why Papa is taking so long to fix his dinner.

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed how the major markets have changed from February, before the start of the Iran war, to now. You can listen to the entire show here. My 8-minute spot with Mike starts around the 57-minute mark.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past six years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.