Trade the price, not the story

The “uncertainty” created by the war in Iran is affecting all of the markets I trade, especially crude oil. I’ve watched videos and read “tons” of theories about why this war is happening, how it’s going, how it will impact other markets, how it will end, and how it will shape the future. There have been considerable “differences of opinion” on all of these issues.

LATE BREAKING NEWS: Saturday night, British Columbia time: Iran has signalled that “friendlies” (China, Korea, India, Japan) can still be assured of “safe passage” via Hormuz. This may be the first indication of “restraint” we’ve seen in two weeks.

I’ve often said that I make money trading not because I have a great crystal ball, but because I’m very focused on risk management. That is especially true in a high volatility market like we have now, where the distribution of “possible outcomes” is very wide.

My first risk management move in this kind of environment is to reduce my trading size. (VOL up / size down). That may mean not trading at all. I’d rather sit tight and protect my capital than trade in wildly volatile markets (because there’s a rumour going around that markets will reopen next week, and there may be lower-risk opportunities then for traders who still have money in their accounts and open minds).

My next risk management move is to “not believe” any story about where the market is going without seeing “validity” from supportive price action that would 1) show me there was some “substance” to the story (or not), and 2) show me “where I would be wrong” if the market moved against me. For instance, I might short a market that has rallied hard with a broad bullish consensus, fallen back a bit, and then rallied again without making a new high, but the broad bullish consensus remains intact. If it starts to turn lower, I can get short, expecting “late to the party” bulls to become sellers, knowing that “I’m wrong on the trade” if the market trades above either the secondary high or the initial high.

Iranian resilience amplifies war duration risk

In last week’s Notes, I wrote that duration risk was a major factor: the longer the conflict lasted, the higher crude prices would rise. I asked, “How resilient is Iran?” Iran may have limited ability to defend itself against aerial bombardment, but if it can (effectively) shut down Hormuz with cheap drones, oil prices may continue to rise.

Why is the market pricing a longer war? My friend Stephen Innes suggests that while “Iran can absorb punishment, it cannot afford humiliation.” If the regime concedes defeat, it loses its legitimacy with the Iranian people. If Stephen is right, this conflict may not end quickly.

Nymex front-month futures rose last week as the market began to price in the effective closure of Hormuz (to any traffic not “approved” by Iran), then absolutely skyrocketed on Monday to ~$120, before collapsing to ~$81, and closing at ~$85 (blue ellipse). Prices dipped to ~$77 on Tuesday, but rallied to close the week at ~$99, the highest weekly close since 2022.

The weekly continuous chart of the front-month futures shows that the market opened and closed at nearly the same price, but traded in a $43 range.

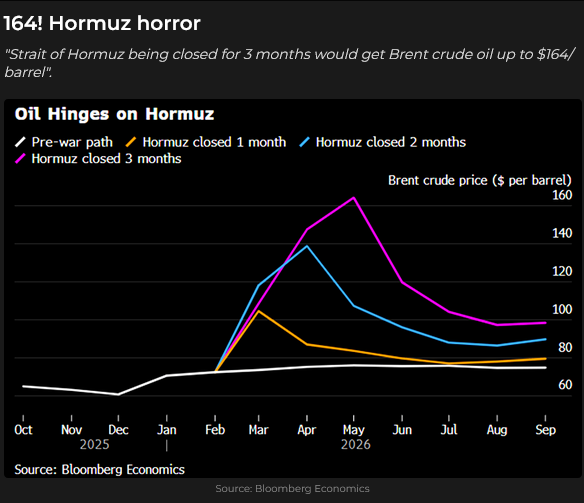

This chart from Bloomberg Economics estimates that if Hormuz is closed for three months, Brent crude could rally to a new record high of ~$165.

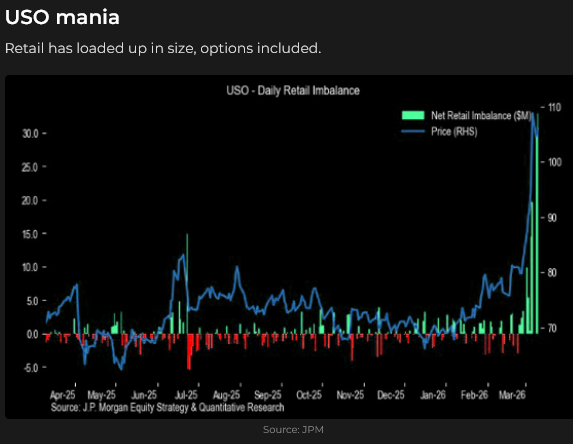

This chart from JPM puts some perspective on recent retail positioning in the USO ETF.

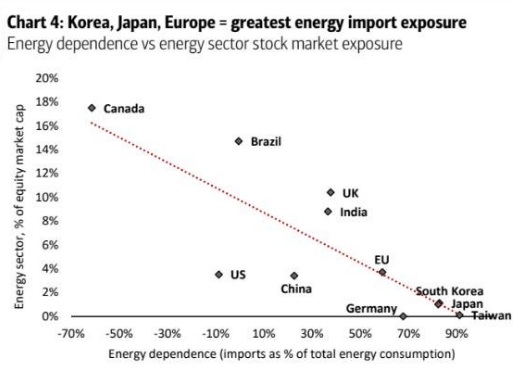

This chart from BoA shows an interesting perspective on the energy dependence of different countries.

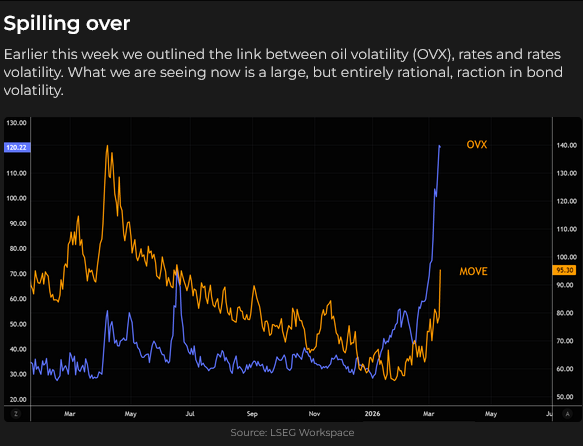

This chart from LSEG Workspace provides a perspective on how the soaring VOL in the crude oil options (blue line) is driving sharply higher VOL in the bond market (gold line).

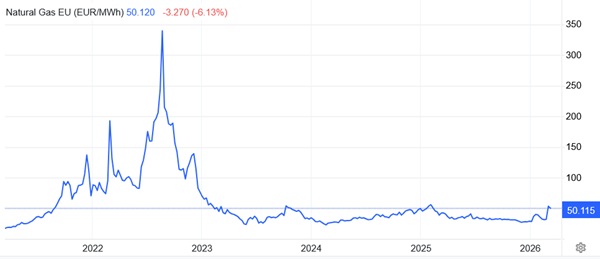

Natural gas prices have jumped in Europe (but not nearly as much as when Russia invaded Ukraine).

Nymex natural gas prices spiked on the cold weather in the eastern USA in January, but have had little reaction to the Iran war.

Currencies

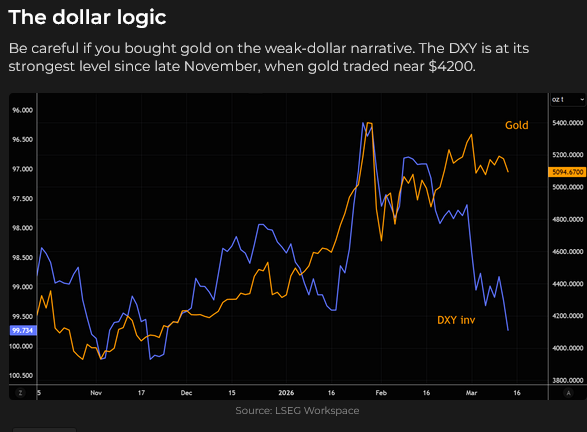

The DXY US Dollar Index is at a 10-month high after rallying ~5% from the 4-year lows it hit in late January when gold and silver were hitting record highs. The US is a net energy exporter.

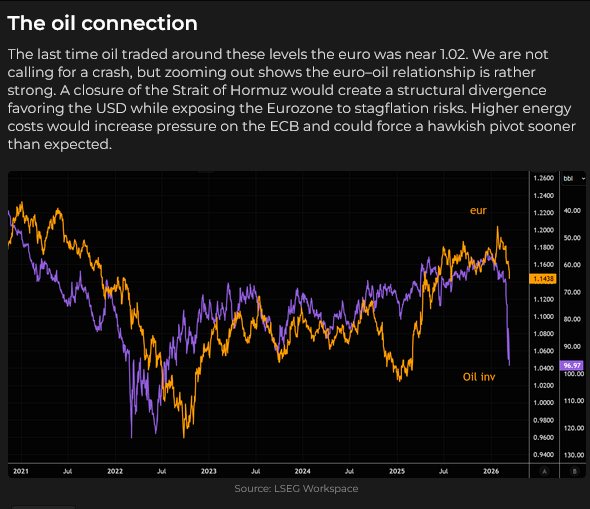

The Euro has fallen to 9-month lows, down ~6% from its 5-year highs in January. Europe is a net energy importer.

This chart shows the Euro (gold line) relative to the crude oil (purple line) price over the last five years. (Note: the oil price is inverted).

The front-month Yen futures (March) closed this week at the lowest level in 40 years (just below the lows of July 2024, which inspired massive intervention by Japanese authorities, causing the Yen to rally by ~16% in two months). Japan is a net energy importer. A weak Yen and sharply higher crude oil prices may increase inflationary pressures in Japan. If there is any sign of a “truce” in the Iran war, the Yen could pop higher on inflation relief and intervention fears.

The Canadian dollar is slightly lower against the USD than it was when the Iran war began. Canada reported much weaker-than-expected employment data on Friday. Canada is a net energy exporter.

Interest rates

The sharp rise in crude oil prices since the beginning of March has heightened expectations of a surge in inflationary pressures. The December 2026 SOFR futures have dropped over 50 bps in the last two weeks, reversing the market’s expectation of 2 x 25 bps cuts from the Fed before the end of the year.

Bond futures prices have dropped by more than five points since the beginning of March, as the 30-year yield has risen from ~4.62 to ~4.90.

Central banks

The central banks of the USA, Canada, Australia, Japan and the Eurozone have scheduled meetings this coming week. While they may express concerns about the surge in crude oil prices, it is unlikely that any of them will raise rates because of it. I do not expect any of the banks to say that they are worried about stagflation. (Sorry, that’s a trader’s idea of humour).

Gold

Comex gold futures have closed lower for both of the last two weeks, with prices down ~$400 from the highs made on Monday of last week. A higher US Dollar and higher interest rates may be weighing on the gold price.

Grains

Grain prices have rallied on concerns that a closure of Hormuz would restrict global fertilizer supplies and boost prices.

Stocks

Global stock markets have trended lower since the beginning of the Iran war. The DJIA reached a record high of 50,500 in early February, but closed this week ~4,000 points lower, a decline of ~8%. This week’s close was a 4-month low.

In addition to worries about the war, rising crude oil prices and possible higher inflation, the American stock indices have been under additional pressure amid concerns about private credit and its impact on the financial sector.

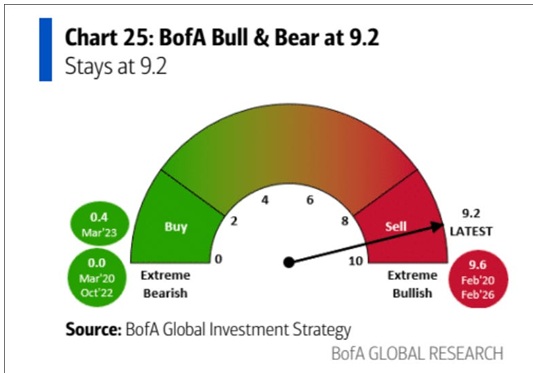

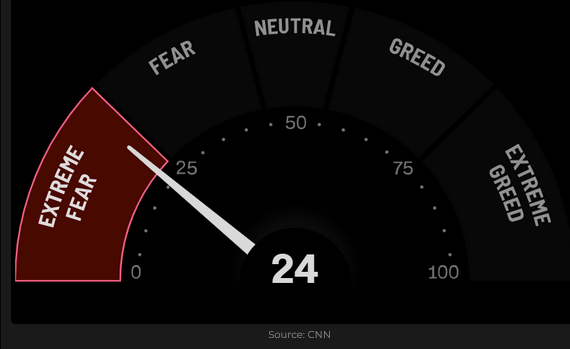

Two weeks ago, investor sentiment was very bullish.

But sentiment has changed dramatically over the last two weeks.

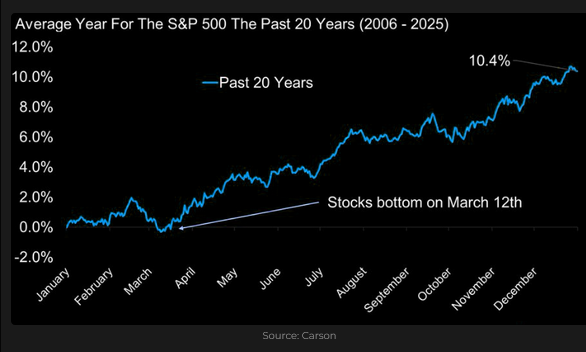

On average, over the past 20 years, the S&P has made its low for the year in mid-March.

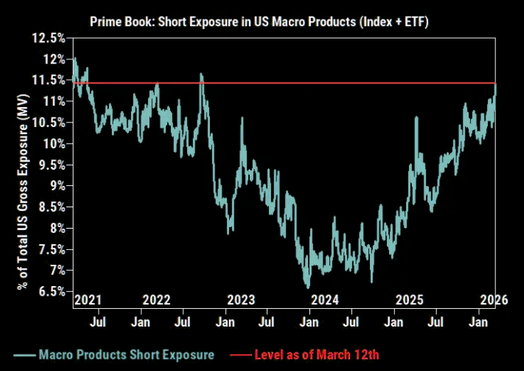

Hedge funds appear to be the most net short macro products they have been over the past five years.

Quote of the week

“Crude oil is worthless until it gets to a refinery.” JJ, alias Alyosha, writing Market Vibes on Substack (I’m a subscriber)

My short-term trading

I’m predisposed to fading crowded market trends. Crude oil fits that description, but managing risk in crude might be tricky, so I looked for a derivative on the oil trade and decided to sell OTM short-dated Treasury Bond puts. As you can see above, VOL on bond futures has jumped, widening the premiums, and bonds have been clobbered for the past two weeks, so I’m willing to sell puts.

The Barney report

I keep telling people that Barney is the happiest dog in the world. Here he is, airborne, at full gallop, with a stick in his mouth. Does life get any better?

Listen to Mike Campbell and me discuss crude oil and Hormuz

On this morning’s Moneytalks show, Mike and I discussed the wild volatility in the crude oil market and its impact on nearly all the markets I trade. My spot with Mike starts around the 57-minute mark. You can listen to the entire show here. Don’t miss Mike’s interview with Robert Bryce about energy markets starting around the 8-minute mark (I subscribe to Robert’s Substack).

The Archive

Readers can access any of the weekly Trading Desk Notes from the past five years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.