Leading global stock indices bounced back this week following the recent “excessive optimism purge”

The S&P reached record highs on October 9, but tumbled on the 10th amid China’s threat to withhold essential rare earths (blue ellipse). The market rallied back on AI enthusiasm and gapped higher over the October 24/25 weekend (pink ellipse) to reach new record highs, but AI doubts remained, and the market drifted lower. The NVDA Quarterly report after the close on November 19 beat expectations on virtually every measure, and the market gapped higher on November 20, only to plunge on heavy volume (orange ellipse), a classic “news failure.” But the market reversed higher the following day on soaring expectations of an FOMC cut on December 10. That rally continued into this week with the market closing higher for five consecutive days.

The “cash” S&P index had a record high weekly (and monthly) close this week.

The DJIA had a record weekly and monthly high close.

The Nasdaq 100 futures contract on the CME closed Friday at its 2nd highest weekly and monthly close.

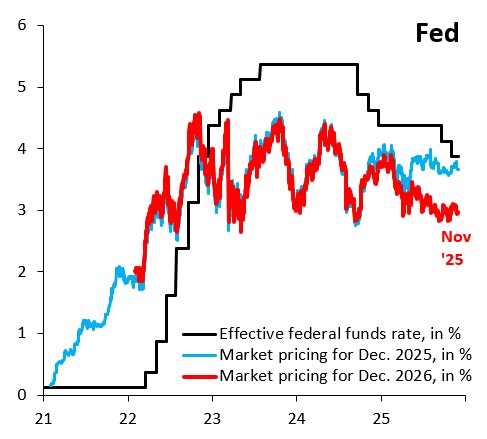

One of the “reasons” for the 5-day stock market rally that started on Friday of last week was the surge in expectations of an “easier Fed”, including 1) an increase in December rate-cut odds to ~85% from ~25% early last week, and 2) increased expectations that Kevin Hassett, currently the head of the National Economic Council, will be nominated for the Chair of the “New Trump-friendly Fed.” (His nomination is expected in December, with the job starting May 15, 2026, following Powell’s retirement.)

Another aspect of the “easier Fed policy to come” idea is expectations for more cuts (~70 bps) in 2026. The Fed previously announced the end of QT on December 1.

Another boost to the stock market came this week with the announcement of the Genesis Mission, an industrial policy on steroids aimed at achieving American energy dominance (a new Manhattan Project). It will provide massive liquidity for the AI/industrial complex as it seeks to reach a new high in American exceptionalism.

The Thanksgiving week is traditionally strong ahead of December, which historically has the largest monthly inflow of capital – hence, the “Santa” rally.

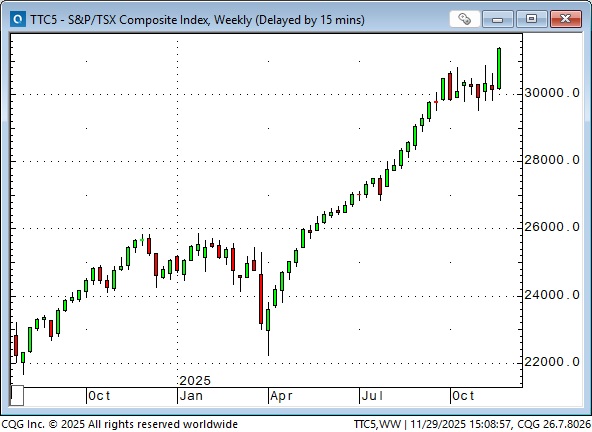

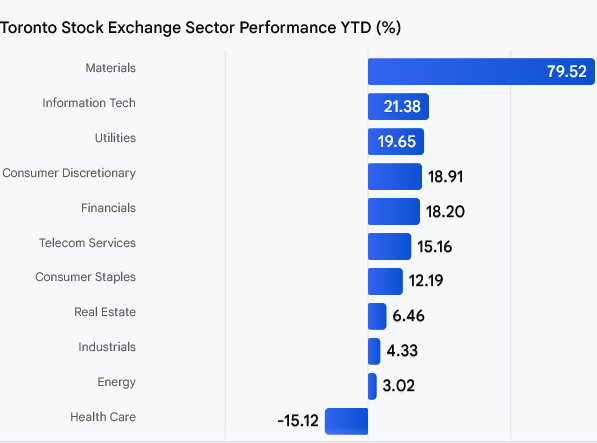

The surging Canadian stock market

The Toronto Composite Index surged to a new record high this week, after drifting sideways in October/November, while the American stock indices weakened. The TSE is up ~25% YTD, up ~40% from the April lows.

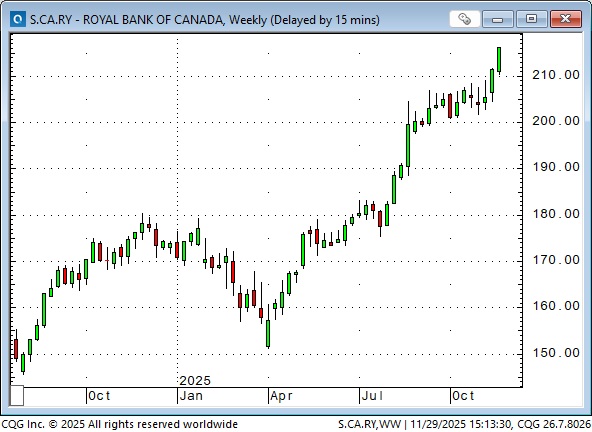

Canadian bank shares account for ~30% of the TSE index’s weighting and have been strong performers. RBC is at record highs, up ~26% YTD, up ~43% from the April lows. (This chart is of RBC on the TSE, in Canadian Dollars.)

Mining shares listed on the TSE have also performed strongly YTD. The XGD is an ETF for gold mining shares listed on the TSE. It had record-high weekly and monthly closes this week.

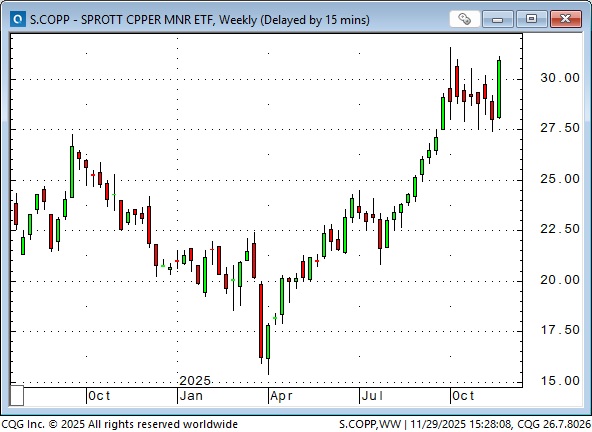

The COPP is an ETF for copper mining shares listed on the TSE. It also posted a record-high weekly close.

Mining companies are included in the “Materials” sector on the TSE.

Mining company share prices have outperformed metal prices YTD (after underperforming last year), as investors pay up for the rising leverage of metal prices soaring relative to production costs. I also believe that some buyers (pension funds, for instance) may want exposure to rising metal prices but (for one reason or another) are prohibited from buying physical metal. Hence, they purchase shares of metal producers.

What about those Canadian pension funds

When I look at the spectacular performance of the TSE Composite (market cap ~CAD $5 trillion), I wonder whether it has been boosted by Canadian pension funds (total assets ~CAD $2.5 trillion) repatriating capital to Canada. There has been “pressure” from the Canadian government for domestic PFs to “invest in Canada.” Still, my Internet searches (Gemini 3) show that the top 8 PFs continue to allocate only ~25% of their total assets to Canada. The largest fund, the CPP (with total assets of ~CAD $720 billion), has only ~12% of its assets in Canada, with ~47% in the USA.

Metals

Comex silver prices soared to a new record high on Friday (on good volume, considering it was a semi-holiday between Thanksgiving Thursday and the weekend). March 2026 is now the lead contract, and it closed above $57 per troy ounce.

Comex copper prices were also strong, with the lead March 2026 contract closing at ~$5.20 on Friday, the highest monthly close in Comex copper history.

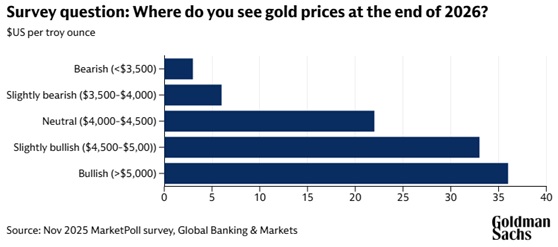

Comex February 2026 gold closed at ~$4,256, up ~$155 on the week (~$150 below the mid-October record highs), setting a record monthly high close for Comex gold.

Currencies

The DXY US Dollar index reached 6-month highs last week, but closed lower each of the past 6 days. There may have been some profit-taking after it failed to follow through on its breakout above 100, and it may also have weakened as cross-currency interest rate spreads narrowed amid market expectations of easier Fed policy.

The Euro closed higher against the USD every day this week.

The Euro fell to an all-time low against the Swiss Franc in mid-November, but bounced back by ~2% at this week’s highs, perhaps in consideration of peace negotiations between Ukraine and Russia. The Euro/Yen cross rate closed at another all-time high.

The Yen fell to an 11-month low against the USD last week (and was only ~1% away from making new 35-year lows), but it rallied a bit this week as the USD slipped against nearly all other currencies.

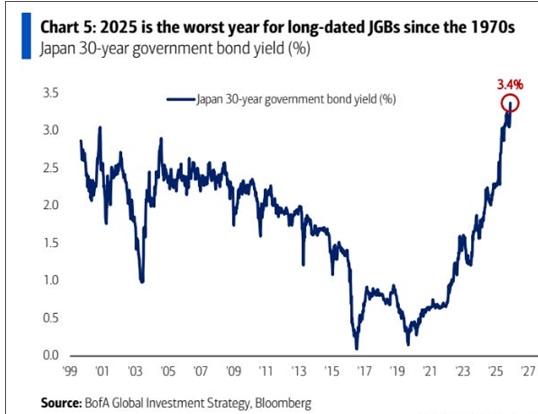

The Yen is weakening as the new Japanese government plans to increase deficit spending to revive the economy. The Japanese bond market (largely freed from the yield curve policies of the BoJ) is doing what you would expect.

The Canadian dollar fell to an 8-week low last week, down ~4% from the June highs, but popped higher this week as the USD was weak across the board. A stronger-than-expected 2.6% GDP report on Friday gave the Loonie an extra lift and likely generated some short covering by speculators.

Interesting charts

Quote of the week

“The uncomfortable reality is that the market is full of terrible investors, wild assumptions, and people who have no idea how fragile the whole structure is. In an environment like this, skepticism isn’t cynicism. It’s self-preservation”. Chris Irons, Fringe Finance

My short-term trading

I didn’t trade much this week, given that I still had a cold and it was Thanksgiving week. After catching a nice chunk of the S&P rally last Friday, I took a poke at the short side on Monday and was quickly stopped for a slight loss.

I bought the Yen on Wednesday as it traded above Tuesday’s highs and kept that (and my Yen “lottery ticket” call options) into the weekend.

I bought the CAD on Wednesday and held it into the weekend, as it rallied nicely on Friday.

My cold seems to be leaving me, so I hope to be more active next week.

The Barney report

It’s the rainy time of year here in the Pacific Northwest Rain Forest, and Barney and I like to go into the forest when we’re out for a walk. There are lots of creatures in the forest, from squirrels and deer to bears and cougars, so it’s nice that Barney is always on alert.

Listen to Mike Campbell and me discuss markets

On this morning’s Moneytalks show, Mike and I discussed the reasons for this week’s sharp stock market rally, the surge in silver and copper prices and the pop in the Canadian dollar. You can listen to the entire show here. My spot with Mike starts around the 51-minute mark.

Mike Campbell’s 2026 World Outlook Financial Conference will be on February 6 & 7 at the Bayshore Hotel in Vancouver. Click here for information and to buy a ticket.

The Archive

Readers can access any of the weekly Trading Desk Notes from the past five years by clicking here.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post new content, typically four to six times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.