Markets assume “Peak Fed Tightening” has come and gone – stocks, bonds, commodities and gold rally, the US Dollar weakens

The Fed raised s/t rates by 75bps Wednesday. The initial market reaction was muted, but during Powell’s press conference, markets decided the Fed would be less aggressive than previously thought – stocks and bonds rallied hard, the yield curve became more steeply inverted, the USD weakened, while gold and commodities rallied.

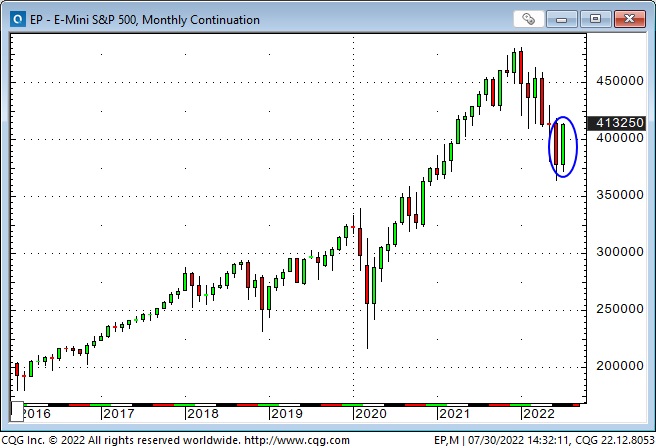

At Friday’s high, the S+P was up ~14% from the June FOMC low, up ~11% over the last three weeks, and up 5% from the lows made Wednesday – before Powell’s post-FOMC press conference.

The DJIA closed Friday up ~2,700 points from the lows three weeks ago, up >1,000 points from Wednesday’s low.

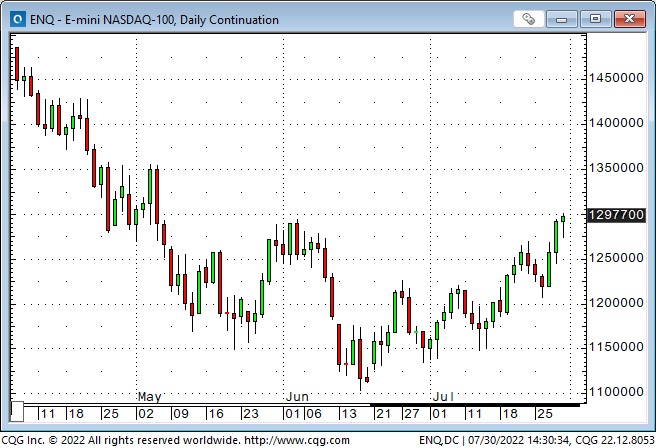

The Nasdaq-100 futures market is up ~18% from the June FOMC lows, hitting the best levels in nearly three months as Mega-Cap tech earnings accelerated the gains created by the change in interest rate expectations. AAPL is up ~26% from the 12-month lows made mid-June.

July’s 420-point S+P rally from low to high was the largest ever monthly rally, outside of the 507-point rally in April 2020 (when the market was recovering from the Covid Crisis – with the assistance of massive monetary and fiscal stimulus!)

Flows and positioning

Market sentiment and positioning around the June FOMC meeting were extremely bearish (the Dow had tumbled ~3,000 points in the two weeks leading up to the June meeting when the Fed raised rates by 75 bps and promised much more to come.) Since the June meeting, markets have dramatically reduced expectations of future interest rate levels (on fears of a Fed-induced recession). While sentiment remained bearish, short covering and FOMO buying accelerated as stock prices rose.

Hat tip to Kuppy

Harris Kupperman (Kuppy) recently tweeted that 2022 has been a disaster for most long-only money managers – that many of these people are facing career risk if they don’t post some good numbers in H2 and CAN NOT afford to miss the current rally. (Classic FOMO.)

Volatility surges as stocks fall – retreats as stocks rise

Basic Vol S+P metrics hit a 19-month high in mid-May as the S+P futures hit a 14-month low. Vol made a lower high on the June FOMC date and trended lower as the S+P rallied.

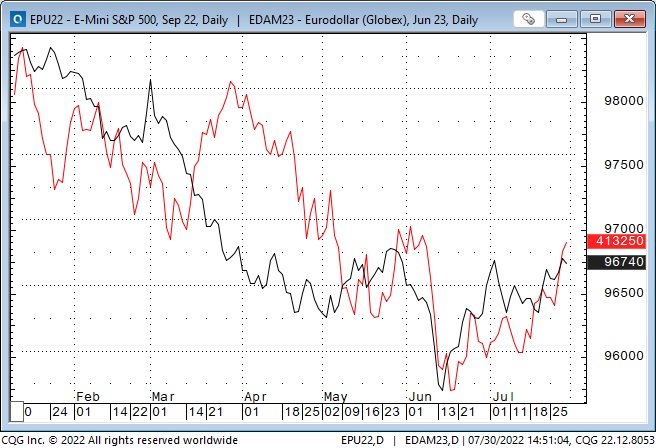

The strong correlation between future interest rate expectations and the S+P

This chart shows the change in the daily closing prices of the June 2023 Eurodollar futures (black line) and the nearby S+P futures (red line.) A falling Eurodollar price = rising interest rates. Both markets have been trending lower YTD, bottomed around the mid-June FOMC meeting, and have been trending higher since. Expectations of future short-term interest rates have had a strong influence on the stock market.

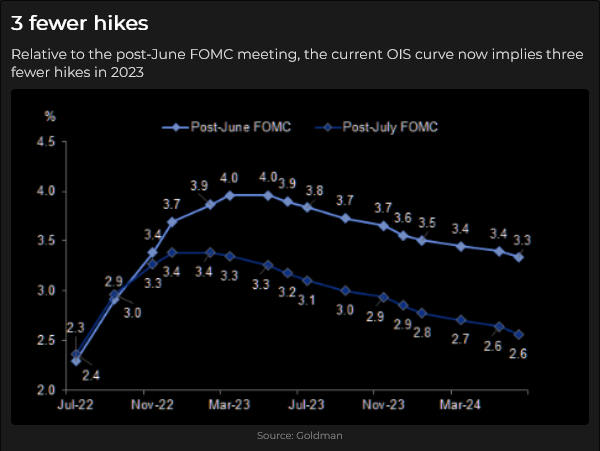

At the time of the June FOMC meeting (which, in hindsight, appears to have been the Peak Fed moment), the market was pricing short rates to top out around March 2023 at ~4%. Following the July FOMC meeting, short rates are expected to top out around December 2022 at ~3.4%.

A big move in the bond market

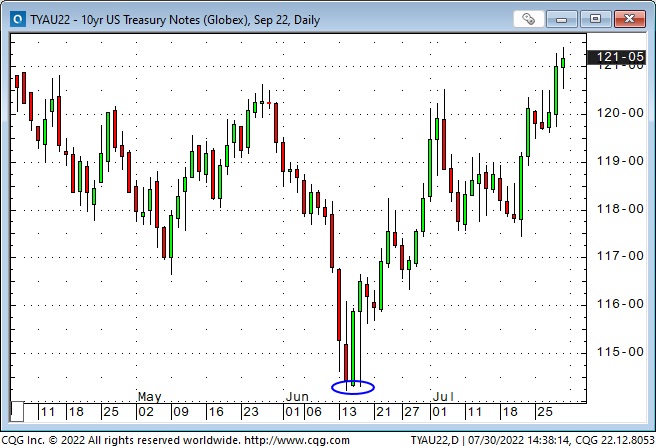

The US 10-year Treasury hit a record low yield of ~0.50% in August 2020 and a 12-year high yield of ~3.5% at the June FOMC meeting. The yield has been falling since then (bond prices rising) and closed Friday at ~2.65%, a 4-month low.

Markets are trying to find a balance between future “inflation expectations” and future “recession expectations”

Powell has promised that the Fed’s determination to bring down inflation is “unconditional,” so markets have to consider that if inflation stays high (current CPI inflation is near 9%), the Fed will continue to push short rates higher (and keep them higher for longer.) But markets also expect a recession (it is already here) and that the higher the Fed takes short rates, the more severe the recession will be – which will prompt/force the Fed to cut interest rates.

Market sentiment ebbs and flows. One month ago, the sentiment was very negative (stocks and bonds were at their lows); since then, stocks and bonds have rallied on the assumption that “inflation expectations” were too extreme in mid-June. If (far too high) inflation is sustained, market sentiment will likely turn gloomy again, and stocks and bonds will fall.

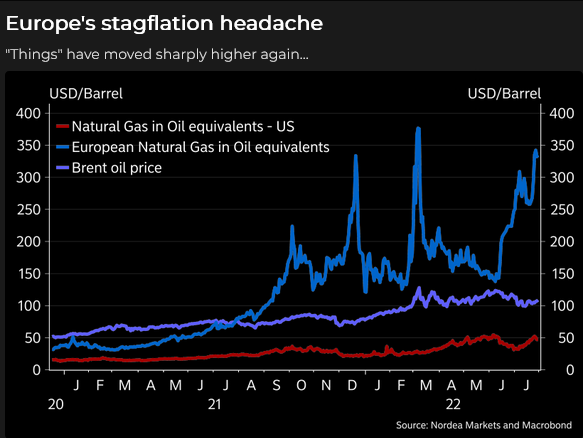

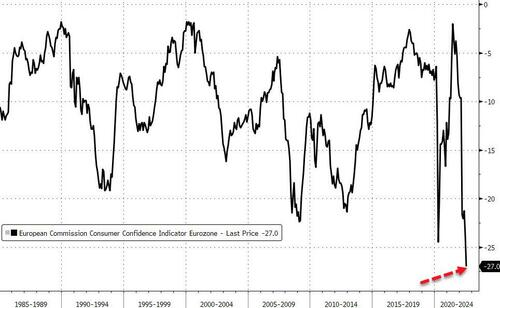

The Eurozone

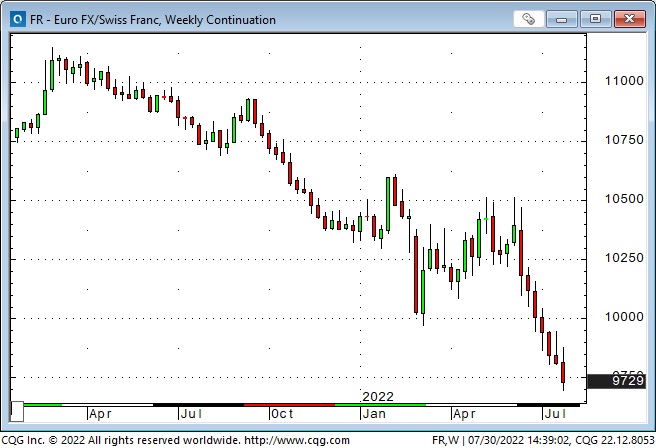

Eurozone CPI inflation is 8.9%. Consumer confidence is at record lows. December NatGas futures are ~8x from where they were a year ago. High energy prices and supply shortages point to rationing and weaker economic growth. The Euro currency is at new All-Time lows against the Swiss Franc (the Euro/Swiss spread is one of my favourite Eurozone stress metrics), and the Euro remains near 20-year lows Vs. the USD.

The US Dollar index has retreated from recent 20-year highs

One of the critical ingredients for a stronger USD has been the perception that the Fed would raise interest rates more aggressively than other leading central banks, and the USDX has accordingly rallied ~20% over the last year. With markets now assuming that Peak Fed has come and gone, the USDX has fallen ~4% from the 20-year highs it reached three weeks ago.

A weaker USD and falling (real and nominal) interest rates have given gold a lift

Gold made All-Time Highs (~$2,080) following the Russian invasion of Ukraine but fell ~$400 to 16-month lows of ~$1,680 on July 21. Gold has rallied ~$90 as the USD and interest rates have fallen. More than half those gains came in the last three days.

Tips are Treasury Inflation-Protected Securities. Rising prices mean that real interest rates are falling. Since 2018, there has been a strong correlation between higher gold prices and falling real interest rates.

Commodity index price action has been (close to) the inverse of the USDX for the past three months

The (energy heavy) Goldman Sachs Commodity Index hit a 20-year low in April 2020 (when WTI prices briefly went negative) and nearly quadrupled to the 12-year highs made following the Russian invasion of Ukraine.

The recent commodity market peak on June 8th was made just as the USDX began to surge higher (from ~1.03 to ~1.09), and when the USDX reversed from a 20-year high on July 14th, the GIC5 also changed course and surged higher.

My short-term trading

I’ve been in “semi-summer holiday” mode for the past couple of weeks and have not traded much. I’ve also been “wrong” in my approach to trading the stock market. I thought it was having a bear market rally (and that may yet be true – depending on your time frame), so I kept looking for opportunities to be short and didn’t have my mind “open” to the possibility that a powerful rally could be taking place.

I’ve previously written that missing a trade “bugs” me more than losing money on a trade, and that has been especially true the past two weeks – I’ve been grumpy!

My primary trading rule is “protect my capital” – the money in my trading account and my mental capital. I’ve done an excellent job limiting my trading losses (my P+L is down less than 0.25% this week), but I’ve been relentless, maybe too severe, in asking myself, “how did I miss buying into this rally?”

In the trading game, there’s an old saying that you learn more from losing than you do from winning, so I hope this introspection turns out to be a good thing.

I’m blessed to have a handful of veteran trading friends that I swap emails with from time to time. Those emails become more powerful and effective the more truthful we are with each other. I used to say that the most effective way to improve your trading was to keep a secret diary about your trading (it should be confidential so that you don’t varnish the truth). Still, I’m beginning to think that swapping emails with trusted and experienced traders may be an even more effective way to improve my trading.

On my radar

It’s easier to have an open mind about where the market may be going if I don’t have to “justify” why I’m holding a position. From that perspective, I have to respect the power of the current shift in market expectations.

Two key questions are, “how much of X is already in the price,” and “what’s my time frame?”

I’ve got a “bias” that inflation will stay higher for longer. Still, I’ve also listened to videos/podcasts and read research/opinion pieces by people I respect who explain why my bias is wrong.

I often think that having an opinion about where a market is going is dangerous, but if I can’t “imagine” that a market could do “X,” then why would I risk taking a position?

My wife and I saw Top Gun this week. On the drive home, I was thinking about what a Little Old Lady I’ve become with my trading (compared to the risk-taking pilots in the movie!) For months, I’ve felt I should step up my intensity and my sizing – but I haven’t been convinced to do so. I’m waiting for that moment to kick in!

The Barney report

Barney and I have been swimming in the ocean every day this week – we’re in the middle of a heat wave. I try to time our arrival at the beach with a low tide which gives us 100 yards of shallow water over a sandy bottom. Barney seems to have endless energy to bound or swim after his ball, but when we get home, he quickly finds a shady spot for a nap!

A request

If you like reading the Trading Desk Notes, please forward a copy or a link to a friend. Also, I genuinely welcome your comments, and please let me know if you’d like to see something new in the TD Notes.

Listen to Victor talk about markets

I’ve had a regular weekly spot on Mike Campbell’s extremely popular Moneytalks show for >22 years. The July 30 podcast is available at: https://mikesmoneytalks.ca.

Subscribe: You have free access to everything on this site. Subscribers receive an email alert when I post something new – usually 4 to 6 times a month.

Victor Adair retired from the Canadian brokerage business in 2020 after 44 years and is no longer licensed to provide investment advice. Nothing on this website is investment advice for anyone about anything.